Much of the debate over teacher pensions is framed as an either/or: Either we keep current defined benefit plans or we shift teachers to low-cost 401k-style defined contribution plans like in the private sector.

In a recent paper with Marisa Vang, we show that this is a false dichotomy. There are cost-neutral alternatives, such as cash balance plans or well-designed defined contribution plans, that could do a better job of providing all teachers with retirement security than the typical defined benefit plan does today.

Yet adopting a wholly different model is not the only option for state policymakers who want to provide more teachers with adequate savings—and that’s probably a good thing, since defined benefit plans are likely to be with us for a while. In our paper, we estimate that under current plans about 80 percent of new, young teachers will leave before qualifying for retirement benefits that meet our definition of “adequate” retirement benefits. This post explores ways to improve that figure using existing defined benefit pension plan structures.

There are two basic ways states could accomplish this. One would be to significantly increase the generosity of current plans. But to reach our adequacy thresholds this way, states would have to increase benefits substantially, essentially doubling the cost of their current plans.

Alternatively, there are cost-neutral ways for defined benefit plans to provide adequate benefits to all workers, but states would have to radically restructure their current plans.

Before diving into those options, let me say a few words about the adequacy target and the test we’re asking teacher pension plans to meet. The adequacy target itself is pretty straightforward. Based on calculations by financial experts on what level of annual saving is needed to afford a comfortable retirement, we established a minimum threshold of 10 percent of savings per year. That includes both the employee and employer contributions, and is in addition to Social Security. (Our paper took Social Security for granted, but 40 percent of public school teachers do not participate in Social Security and thus rely solely on their pension plan. Readers should keep this in mind, as it does play an important role in how we should think about the adequacy of teacher retirement benefits.)

Last, we focused our paper on the retirement benefits provided to teachers who begin their careers at age 25. This is a fairly typical entry point for new teachers, but it represents a hard test for pension plans. Due to the way teacher pension plans work today, teachers who enter the profession at younger ages have to stay much longer to qualify for adequate benefits and have the most to gain from a more progressive benefit structure. Since we assumed a five-year vesting period for all the models in our paper, I’m using that threshold again here.

Let’s look first at how to achieve adequacy through benefit enhancements, and then turn to how to achieve adequacy through restructuring.

Achieving Adequacy Through Benefit Enhancements

Until quite recently, the history of teacher pension plans was primarily one of benefit enhancements. States created their plans decades ago, and many featured all-or-nothing provisions, where the benefits were designed solely for long-serving veterans. Over time states enhanced those benefits by reducing vesting periods, raising multipliers, and lowering normal retirement ages. This trend peaked in the year 2000, when the median state pension plan was fully funded, and state legislators pursued significant benefit enhancements.

Since then, as states have grappled with growing unfunded liabilities, they’ve gone through several rounds of benefit cuts and the creation of new, less generous benefit tiers for newly hired teachers. As we documented a couple years ago, retirement benefits are, on net, worse for new teachers starting out today than any time in the last 30 years. That trend has only continued since.

But what if we were to reverse these trends? What would it take to get all vested teachers up to a minimally adequate retirement savings target?

To model this out, I started with a very simple baseline pension plan. I assumed that workers were eligible for a pension worth 2 percent multiplied by their years of service and their average salary over the final three years of their career, that they vested in the system after five years of teaching, and that they became eligible to collect benefits at age 60. (See my full assumptions at the end of the post.)

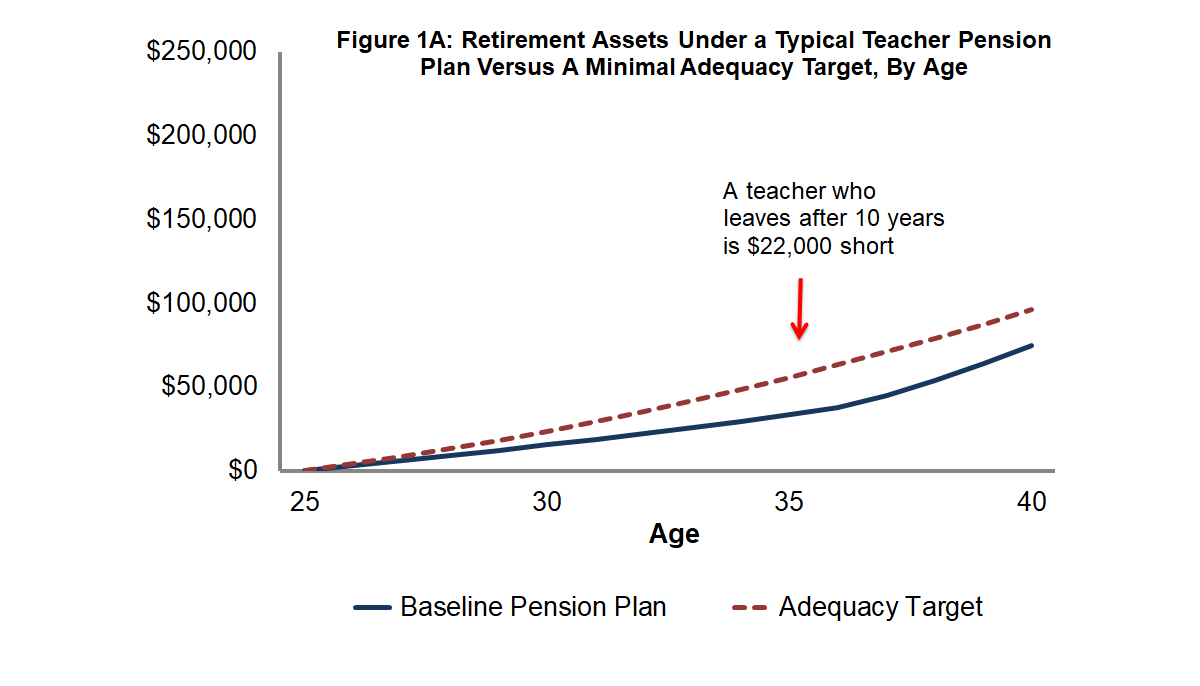

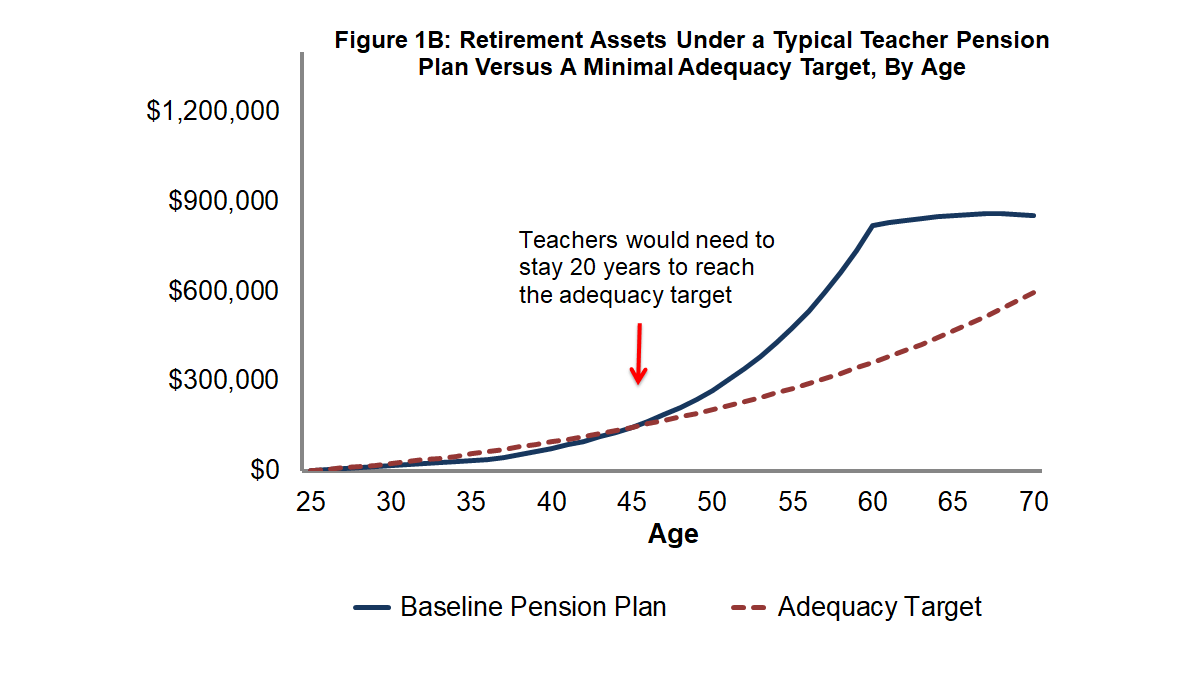

In Figures 1A and 1B below, the solid blue line in both graphs shows how benefits would accumulate under this plan. (For each figure in this post, version A focuses in on teachers between the ages of 25 and 40, who comprise the bulk of those failing to hit adequacy targets under current plans. Version B then shows the same data for the full age distribution.) As a point of comparison, the red dotted lines show the minimal adequacy target from the paper, equivalent to someone saving 10 percent of their salary each year from personal as well as employer contributions and earning a 4 percent real rate of return on their investments. In this model, it would take teachers 20 years of service to reach the adequacy target, after which their pension values would increase substantially.

Consider someone who starts at age 25 and leaves after 10 years of teaching. She will qualify for a pension, but she won’t be able to collect it until she reaches age 60, and it will be based on her salary in the year in which it was earned. Compared to the adequate savings target, this teacher will have retirement assets $22,000 less than what she should have saved to be on track for a comfortable retirement. If she continues teaching her pension value will eventually more than surpass the adequate savings target, but the risk is that she’ll leave before then. In fact, as Figure 1B shows, teachers would have to stay 20 years before qualifying for benefits that meet the minimal adequacy threshold.

This arrangement will work out fine for some teachers, but most teachers will fall short. To afford a comfortable retirement, teachers who fall short of the adequacy targets will have to work longer, save more in their personal accounts, or rely on other forms of income in their retirement years.

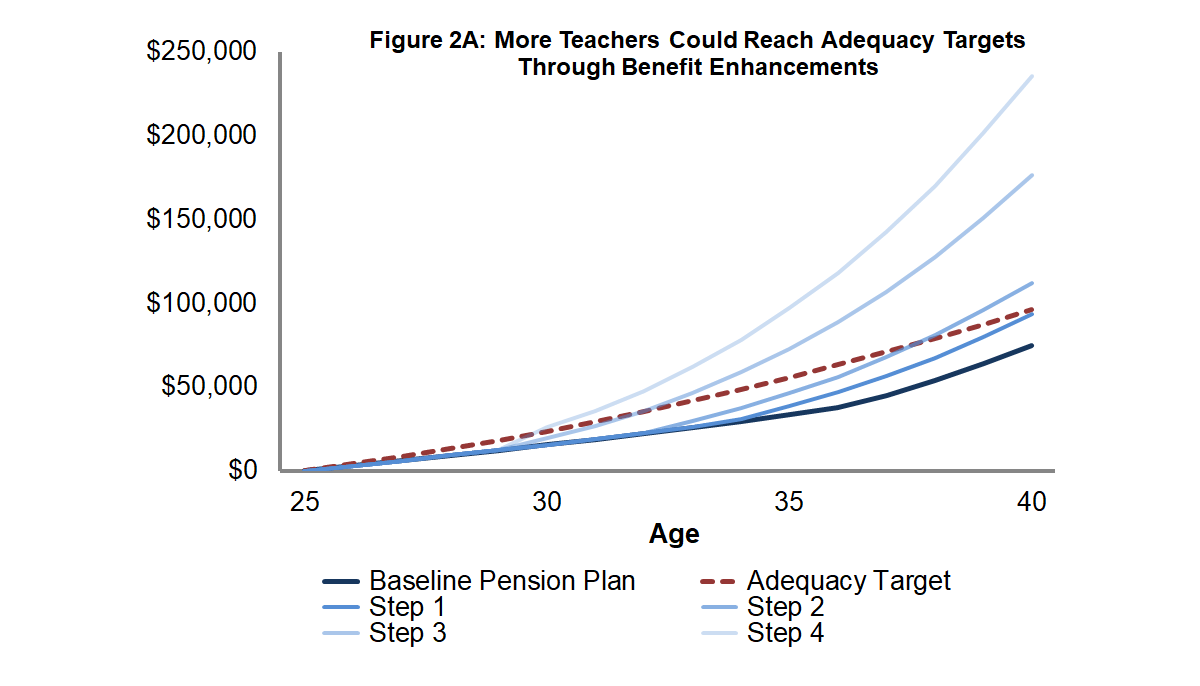

This baseline model assumes the total cost of the plan to be equivalent to 12 percent of a teacher’s salary. States could provide all vested teachers with adequate benefits though benefit enhancements, but it would require roughly doubling the contribution rate. Although states could pull these levers in different combinations, here’s one way to get there:

Step 1: Increase the multiplier from 2.0 to 2.5 percent. Teachers would reach the adequacy point by year 16, but contribution rates would need to rise by 2.4 percentage points.

Step 2: Further increase the multiplier from 2.5 to 3.0 percent. Teachers would reach the adequacy threshold by year 13, but contribution rates would be 4 percentage points higher than the baseline.

Step 3: Keep the multiplier at 3.0 percent but drop the normal retirement age to 55. Teachers would reach the adequacy threshold by year seven, but contribution rates would be 8.5 percentage points above the baseline.

Step 4: Keep the normal retirement age at 55 and increase the multiplier to 4.0 percent. All teachers would reach the adequacy threshold by the time they vest in year five (success!), but contribution rates would need to be 11.9 percentage points above the original baseline.

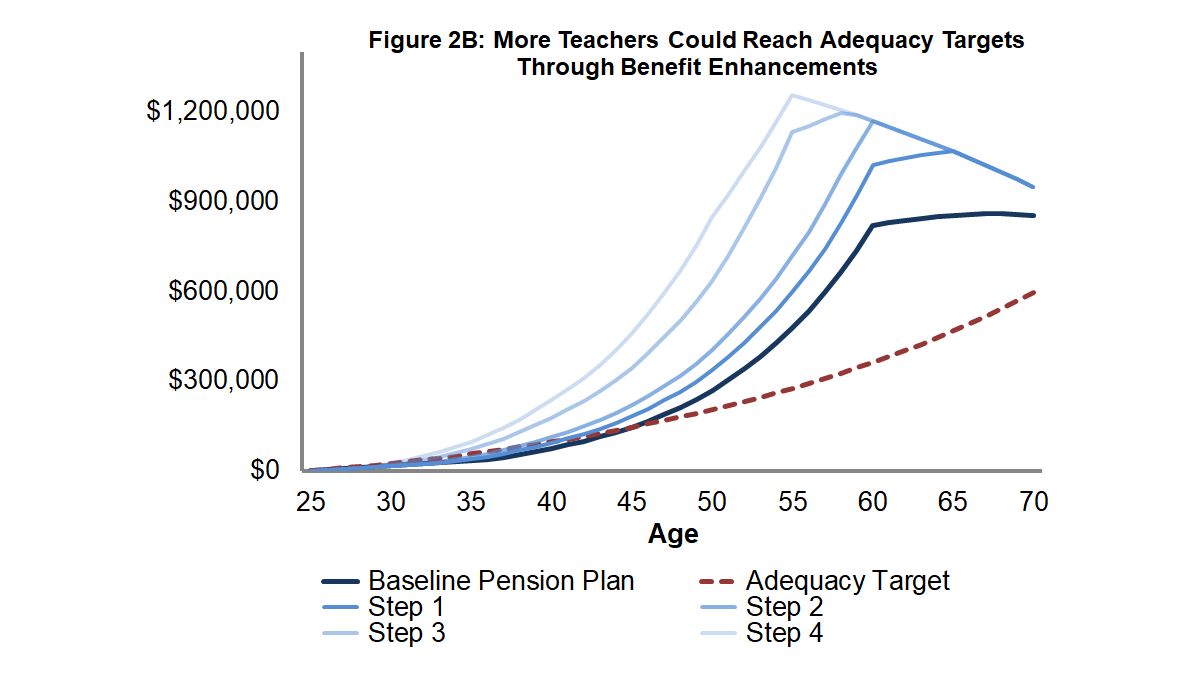

Figures 2A and 2B below show how benefits would accumulate at each of these steps. As before, the dark blue lines represent the original baseline defined benefit plan, the dotted red lines represent the adequacy target, and the lighter-colored lines represent steps 1-4. As the graphs show, these steps have pushed all vested teachers above the adequacy target, but in a highly inefficient manner. For example, the retirement assets of a five-year veteran would rise by about 69 percent, an increase worth about $11,000 in lifetime retirement wealth for that teacher. But as Figure 2B shows, a 30-year veteran who reaches age 55 would have seen the value of her pension increase by 163 percent, or almost $800,000.

This inefficiency may explain why no state has gone anywhere near this far with their defined benefit pension plans. But these are the same levers that states pulled when their finances were in better shape. If anything, states sought to keep costs down somewhat by focusing their spending even more on long-term veterans, through multipliers that increase only after certain longevity thresholds (say 20 or 30 years) or retirement thresholds tied solely to years of service (rather than age). In other words, my example here is extreme, but not because states weren’t trying to get there.

Achieving Adequacy Through Restructuring

There is another way to provide all teachers with adequate retirement benefits through traditional defined benefit pension plans, but the usual tweaks to the basic benefit formulas won’t work. It would require more radical changes that address the root causes of the problem with existing defined benefit plans–the fact that they are regressive and disproportionately reward long-serving, higher-paid workers.

States could choose to boost their benefits to early- and mid-career teachers by adjusting their rules on the refunds they provide to departing teachers. Currently, teachers who leave a given pension system are able to claim a refund on their own contributions, but in only a few states are they eligible for any of their employer’s contributions. Moreover, most states set their interest credits on the teacher’s own contributions quite low—they could at least peg their credits to their actual investment returns. Still, without any employer match, the only way to get a standard defined benefit plan above the adequacy threshold would be to increase employee contribution rates above 10 percent.

States could help more teachers by offering an employer match on teacher contributions. Just six states offer their teachers any match today, and most of those are partial matches. Colorado and South Dakota come the closest to our target, but even they fall short. South Dakota, for example, provides a 50 percent employer match for non-vested workers and an 85 percent match for vested workers. However, it sets its interest credit at less than short-term Treasury bills, meaning departing workers are getting a match but no real interest on their contributions. Colorado has fixed its interest credit at 3 percent, which is better than a savings account but barely more than inflation, and certainly not enough for long-term retirement savers.

While these types of changes would benefit teachers, I wanted to see if I could reach the adequacy goal solely through modifications to the benefit formula itself. My goal was to ensure all teachers qualified for the adequacy threshold by year five, at no additional cost to the plan.

Essentially, I had to find a way to smooth out the benefits awarded under the baseline defined benefit. First, I lowered back-end benefits by increasing the normal retirement age to 65, lengthened the period over which an employee’s salary was averaged from three years to 10, and introduced a benefit cap of 80 percent of the worker’s final average salary. These changes may sound extreme, but they are directionally similar to the benefit cuts for new teachers that states have adopted in recent years to control costs. They also made it possible to increase the multiplier from 2.0 to 10.0 percent without increasing overall costs. Combined, these changes dramatically increase the share of workers who would receive adequate benefits.

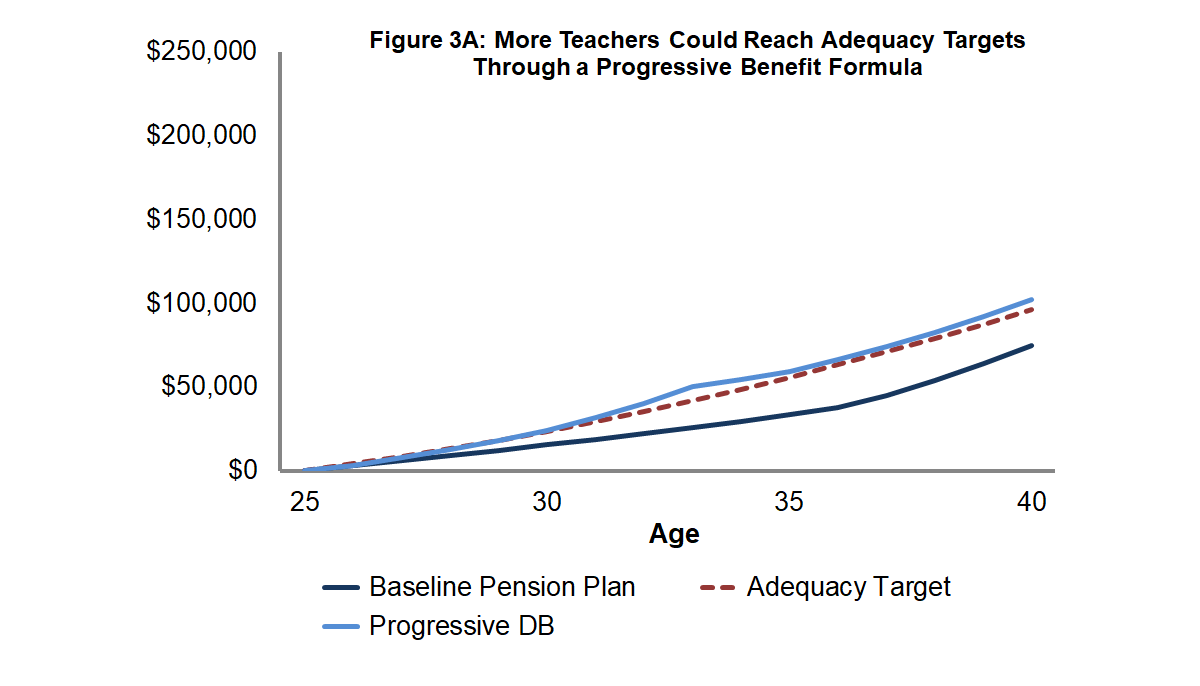

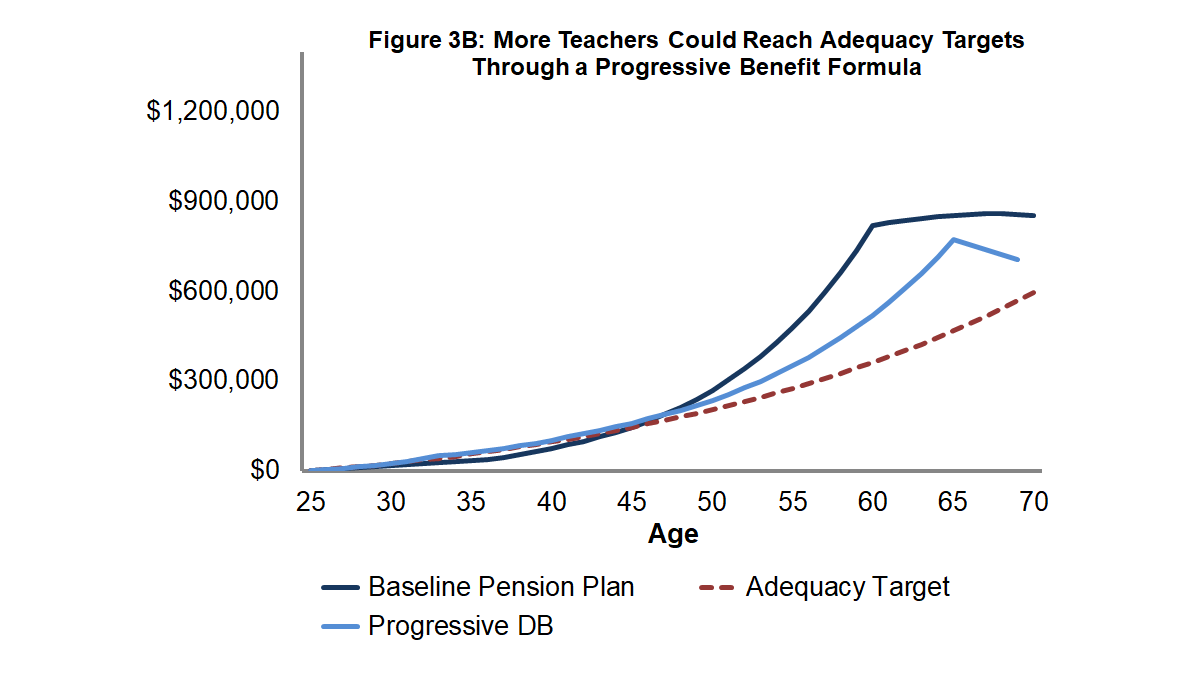

Figure 3A and 3B show what the results look like visually. As before, the dark blue lines represent the baseline defined benefit plan, and the dotted red lines show the adequacy target. In these graphs, the blue lines show the results of what I call a “Progressive Defined Benefit” plan. They illustrate how a defined benefit plan could be designed in such a way to provide adequate retirement benefits to all vested teachers. This type of design deliberately trades away some back-end rewards in order to increase the chances that all entering teachers would leave their years of service with adequate retirement benefits. (Remember, this exercise is looking only at future teachers. I do not recommend states change the benefits already earned by current teachers or retirees.)

Takeaways

The choices I’ve offered here are intended as illustrative examples. I’ve shown that it is possible to re-design defined benefit pension plans so that they offer adequate retirement benefits to more teachers. However, if state leaders agree on that goal, they must be willing to pay higher costs to meet it, or else they must radically re-think their current benefit structures to reach that same goal without ballooning costs.

Reasonable people can disagree with the specific adequacy target I’ve chosen or how to interpret the results. Some might argue my target is too high, although they would be implicitly suggesting that teachers who fall short of the target should make up the savings some other way, such as relying on a spouse, saving more at another job, or just surviving a less-than-comfortable retirement.

Others might argue we should reserve scarce public resources for the longest-serving veterans. That view might sound reasonable, but the exercise here demonstrates that there are ways to provide all teachers with adequate benefits within existing structures.

On the other hand, I imagine some readers might ask why we should go through all this trouble to re-fashion defined benefit pension plans when other alternatives are available. As we write in our recent paper, defined contribution and cash balance plans could easily be designed to ensure all workers had adequate savings regardless of their years of service. Those alternative plans would also have financial benefits. Due to decades of over-promising and under-saving, teacher pension plans today are under-funded by $500 billion, and rapidly rising pension costs have contributed to the stagnation of teacher salaries. These problems are unique to defined benefit pension plans, and these funding issues could be avoided if states transitioned to other types of retirement plans.

I’m sympathetic to these arguments, but I also realize that defined benefit pension plans will be with us for a while, and I’d rather states design their retirement plans to serve all of their workers as well as they possibly can. In the meantime, I hope this exercise leads more policymakers to question whether their state’s retirement plan meets the needs of all teachers, who they might be leaving out, and how those plans could be improved.

Chad Aldeman is a principal at Bellwether Education Partners

Assumptions

| Baseline Defined Benefit (DB) | Step 1 | Step 2 | Step 3 | Step 4 | Progressive DB | |

| Starting Salary | $40,000 | $40,000 | $40,000 | $40,000 | $40,000 | $40,000 |

| Salary growth rate | 3% real | 3% real | 3% real | 3% real | 3% real | 3% real |

| Employee contributions | 7.5% | 7.5% | 7.5% | 7.5% | 7.5% | 7.5% |

| Employer contributions for benefits | 4.5% | 6.9% | 8.5% | 13% | 16.4% | 4.5% |

| Investment return assumption | 7.5% | 7.5% | 7.5% | 7.5% | 7.5% | 7.5% |

| Inflation assumption | 3% | 3% | 3% | 3% | 3% | 3% |

| Vesting period | 5 years | 5 years | 5 years | 5 years | 5 years | 1 year |

| Multiplier | 2% | 2.5% | 3% | 3% | 4% | 10% |

| Final Average Salary (FAS) | Highest 3 years | Highest 3 years | Highest 3 years | Highest 3 years | Highest 3 years | Highest 10 years |

| Benefit Cap | 100% of FAS | 100% of FAS | 100% of FAS | 100% of FAS | 100% of FAS | 80% of FAS |

| Normal retirement age | 60 | 60 | 60 | 55 | 55 | 65 |

| COLA | 2% | 2% | 2% | 2% | 2% | 2% |