As charter schools across the country struggle to keep up with demand, a new federal tax incentive could hold the key to spurring billions of dollars in investment in low-income areas with limited access to quality public charter school options.

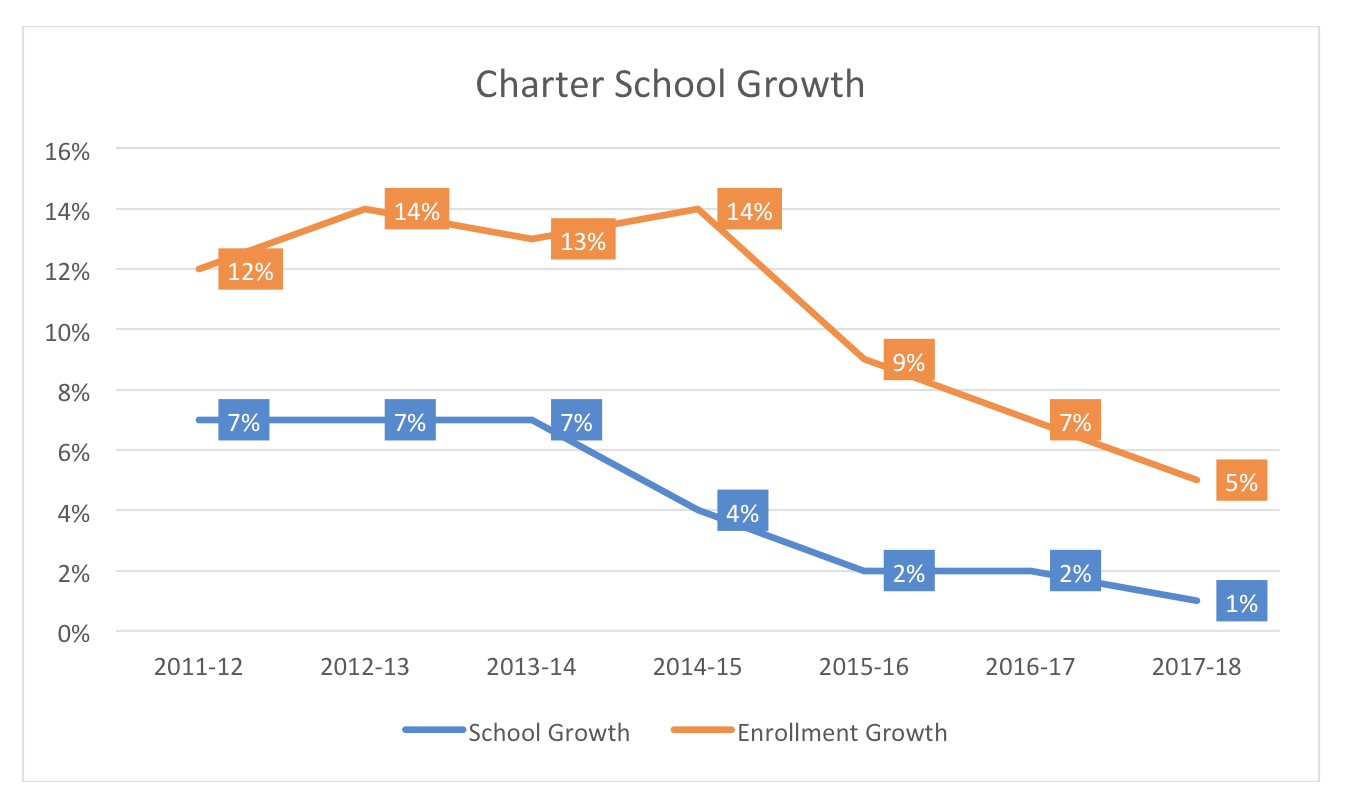

Despite educating more than 3.2 million students, the annual rate of charter school growth has reached an all-time-low – a 1 percent increase in charter schools during the 2017-18 school year. This represents the fourth consecutive year that charter growth has slowed.

Source: National Alliance for Public Charter Schools annual estimates.

Yet, there are still millions of children with limited access to a high quality public charter school. A 2017 Brookings Institution analysis by Matthew Chingos and Kristin Blagg found that only 46 percent of families have a charter school within 5 miles from their home. And a recent Fordham Institute analysis finds there are over 500 medium- and high-poverty Census tracts across the country without nearby charter elementary schools. Dubbed “charter school deserts,” these areas are predominantly located in urban and rural settings and represent populations of students in most need of alternative school options.

One of the biggest obstacles to charter school growth is securing affordable school facilities. Unlike district schools, which have the power to tax and issue taxpayer-backed bonds, charter schools rely on a hodgepodge of facilities supports and must often resort to digging into their per-pupil instructional budget to pay for facilities.

While states can and should continue to create facilities options for their charter schools, a new federal tax incentive has the potential to lighten that load for hundreds, even thousands, of charter schools across the country.

The Opportunity Zone program was enacted as part of the 2017 tax reform package. The program was designed to encourage investments in low-income areas left behind by the economic recovery. Over the past few months, governors have been nominating up to 25 percent of their low-income Census tracts as Opportunity Zones. Final nominations were due to the Department of the Treasury on April 20th, which has 30 days to approve submissions.

To create a mechanism to invest in these areas, the legislation authorized the creation of Opportunity Funds, which are required to invest at least 90 percent of its assets into Opportunity Zone communities.

To encourage development in these distressed communities, investors in Opportunity Funds are given significant tax benefits for holding their investments for five, seven, and ten years. The example below illustrates the significance of the benefits.

Example of Tax Savings for Opportunity Zone Investments

Imagine an investor purchased stocks for $200,000 that appreciate over time to $1 million. If the investor was at the top tax bracket, the $800,000 in capital gains would typically be taxed at a rate of 20 percent plus a 3.8 percent surtax when they sell the asset.

If this $800,000 in capital gains was instead invested into an Opportunity Fund for five years, 10 percent of the deferred $800,000 would be forgiven for tax purposes. If held in an Opportunity Fund for seven years, 15 percent would be forgiven. Meaning, if the $800,000 in capital gains were invested for at least five or seven years, only $720,000 or $680,000 would be subject to tax, respectively [10 percent and 15 percent subtracted from $800,000].

As significant as this tax benefit is for distressed communities, it gets even better. If capital gains are invested in Opportunity Funds for at least ten years, the 15 percent tax forgiveness applies as well as tax forgiveness on any gains made in the Opportunity Fund investment. So, imagine that the taxpayer above invested their $800,000 in capital into an Opportunity Fund, held it for ten years, and saw it appreciate to $1.2 million. The taxpayer would continue to see a 15 percent tax forgiveness on the $800,000 investment (taxed at $680,000) and would not be taxed on any of the $400,000 gained through the Opportunity Fund investment.

This is a significant tax benefit directed to spur investment into the thousands of distressed communities across the country that have not recovered since the Great Recession. Brookings’ Adam Looney notes, “Individuals in a high-tax state and with short-term capital gains can avoid $7.50 in taxes for each $100 they invest, even before considering any return on their Zone investments.”

Given that there is an estimated $6 trillion in unrealized capital gains in the U.S., this has the potential to be the largest economic development program in our nation’s history. As the American Enterprise Institute’s John Bailey recently wrote, “This should allow distressed communities to tap a multi-trillion-dollar pool of capital to support a wide range of economic development activities. Funds could be broad or narrowly focused, with an emphasis on a single sector, such as housing development, charter school facilities, or broadband expansion.”

Comparing the Opportunity Zones to the New Markets Tax Credit Program

Charter advocates were up in arms late last year when the New Markets Tax Credit (NMTC) faced elimination as a result of tax reform negotiations in Congress. The NMTC program is an existing federal incentive to attract investors into low-income communities. Investors receive a 39 percent tax credit on their investment if they hold it for at least seven years. Charter schools across the country rely on NMTC funds for financing affordable facilities.

To put the Opportunity Zone program into perspective, it helps to compare it to the NMTC program, that was enacted in 2000.

Scale. The NMTC requires an annual appropriate from Congress, which over the past several years has been a total of $3.5 billion. The Community Development Financial Institution (CDFI), which oversees the program, estimated that through May 2017, the NMTC program has awarded around $43 billion in NMTC, with about $2.2 billion going toward charter schools.

Compare that to the $6 trillion in unrealized capital gains that could be tapped through Opportunity Zones. If just one-tenth of one-percent of these funds find their way into charter school development projects, that would mean $6 billion in new capital going towards charter construction – nearly three times the amount of investment that the NMTC program spurred over more than a decade.

Complexity. While Treasury is in the process of setting up the rules that define how Opportunity Funds can be set up and funds invested in Opportunity Zones, the intent of the enacting legislation makes a clear distinction from NMTCs.

The NMTC program was exactly that – a program. In addition to the annual allocation required by Congress, the NMTC program is run by CDFI staff who review applications for tax credits through a competitive grant process. In fact, many consultants advertise their ability to successfully win NMTC awards.

Opportunity Zones, however, are better described as a new tax rule that simply changes how capital gains are treated once reinvested into an Opportunity Fund.

Opportunity Zones and Charter Deserts

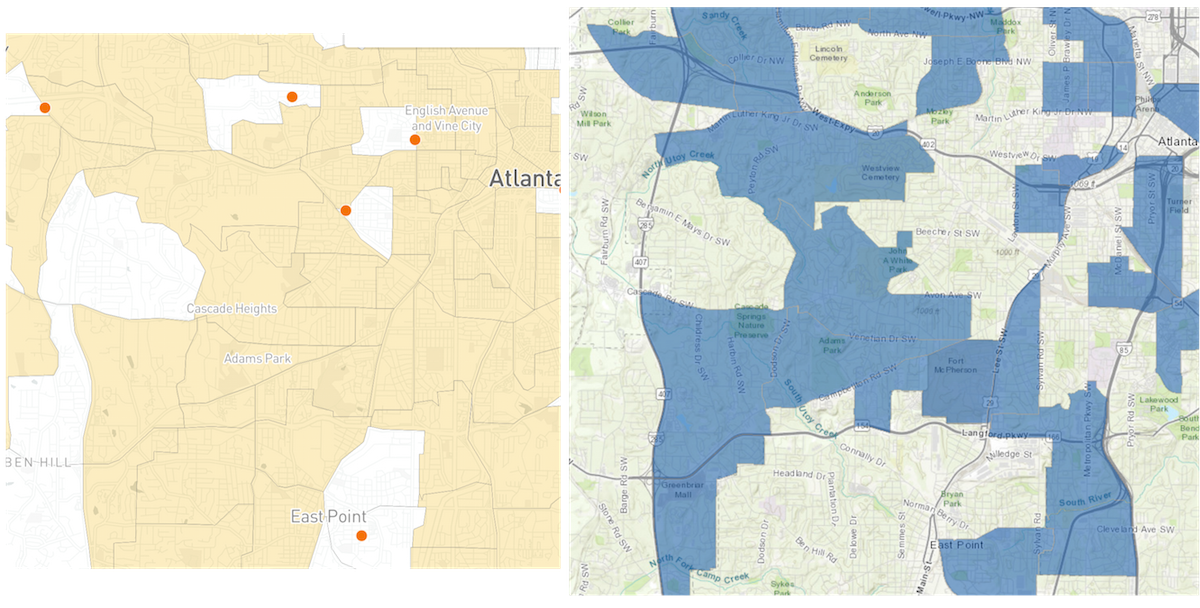

The Fordham Institute report on charter deserts in instructive for how capital could be deployed. An interactive map shows the charter deserts in each area of the country, as well as pinpoints for where charter elementary schools are located.

Meanwhile, CDFI has an interactive map showing designated Opportunity Zones across the country.

Take, for example, the two images below. The image to the left is Fordham’s map of charter deserts (Census tracts) in Southwest Atlanta highlighted in orange with darker orange dots representing charter elementary schools. The image to the right is a map of roughly the same area, except highlighting Opportunity Zones in Southwest Atlanta in blue.

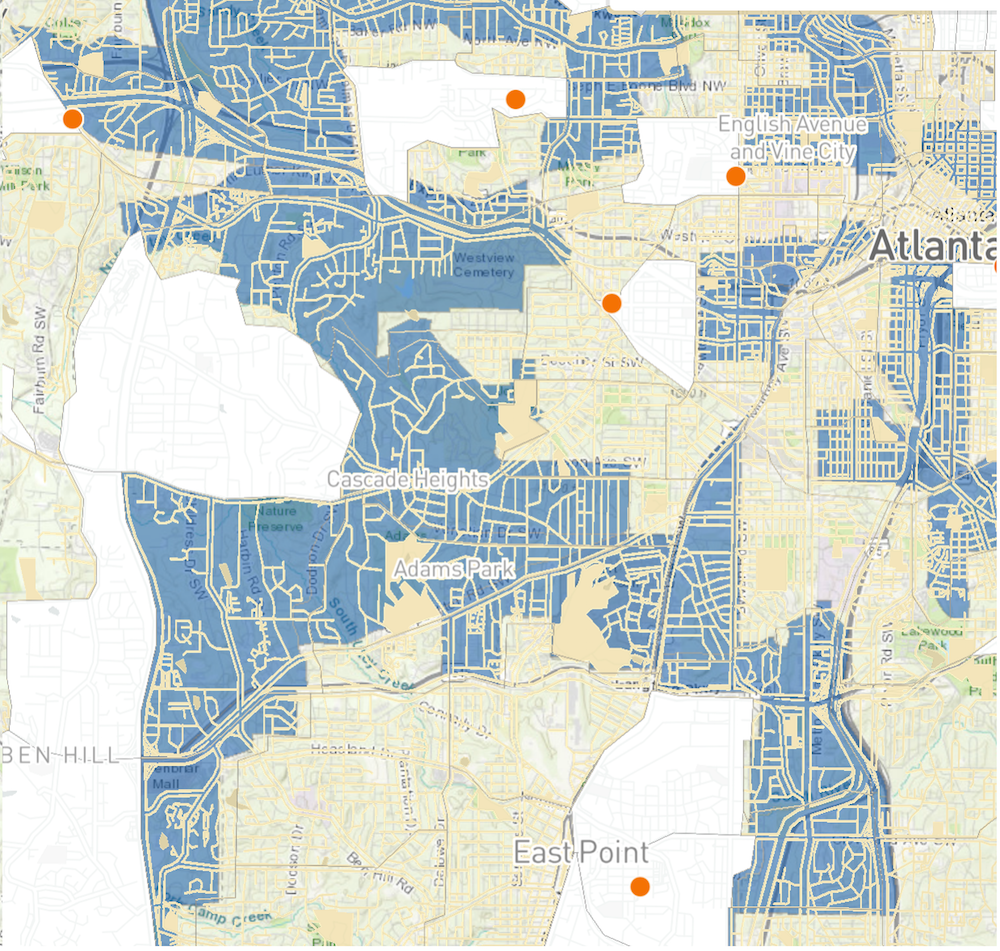

By merely overlaying the map of Opportunity Zones onto Fordham’s Charter Desert map, you find areas that are both Charter Deserts and Opportunity Zones (represented as the areas shaded in blue in the map below). These are communities that are ripe for philanthropic investment for new charter schools.

That is not to say that each of these communities needs a charter school located within its boundaries. Especially in dense urban areas, transportation efficiencies may not necessitate a brick-and-mortar school in every neighborhood. Additionally, the case could easily be made for charter schools in areas that are neither Charter Deserts nor Opportunity Zones.

However, philanthropy has invested billions of dollars into equalizing charter facilities costs. One can imagine how many of these organizations could use their limited philanthropic capital to access a deeper pool of private capital for charter facilities – creating long-term, stable funds for high quality charter schools to draw down from.

Opportunity Zones were created to incentivize long-term investments into economically distressed areas. Surely there are few better investments than creating high quality public school options that can change the trajectories for children and their communities.

— Adam Peshek

Adam Peshek is Managing Director of Opportunity Policy at ExcelinEd.