Video: Frederick Hess on funding innovation

In Education Unbound, Frederick Hess, director of education policy studies at the American Enterprise Institute and Education Next editor, argues for new education service-delivery organizations that, free from the constricting norms and rules of traditional providers, focus single-mindedly on executing their model. The challenge for reformers is to recognize that enabling such providers is not just a matter of promoting “school choice,” but also of freeing up the sector to a wealth of different approaches and cultivating conditions in which problem solvers can succeed and grow. Hess argues in the selection below that funding is the fuel required for innovators to thrive.

Greenfield is a term of art typically used by investors, engineers, or builders to refer to an area where there are unobstructed, wide-open opportunities to invent or build.

— Chapter 1, Education Unbound

From Education Unbound: The Promise and Practice of Greenfield Schooling (pp. 114–125), by Frederick M. Hess, Alexandria, VA: ASCD. © 2010 by ASCD. Reprinted with permission.

New ventures can neither launch nor grow without money. In the absence of funding, greenfield efforts become soul-sucking endeavors for their founders, proceed much more slowly than necessary, or never get off the ground at all. The famous KIPP academies almost died before seeing the light of day because founders Mike Feinberg and David Levin had trouble assembling the few thousand dollars they needed to get started. Raising those funds required the two to write scores of letters and make countless appeals to Houston-area donors. As Washington Post reporter Jay Mathews has wryly recounted in his colorful history of KIPP, Work Hard, Be Nice, “Out of more than one hundred letters, only about a third responded. Most said, in polite corporate language, that they had never heard of KIPP and didn’t like the sound of it. None promised money.”

Teach For America’s Wendy Kopp also struggled to find funding when launching TFA. She has described [in Public Affairs] being schooled by Princeton faculty in just how hard it would be to raise the requisite funds, remembering, “What [Professor Bressler] really wanted to know, he said in his booming voice, was how in the world I planned to raise the $2.5 million…. He didn’t seem convinced. ‘Do you know how hard it is to raise twenty-five hundred dollars?’ he asked.”

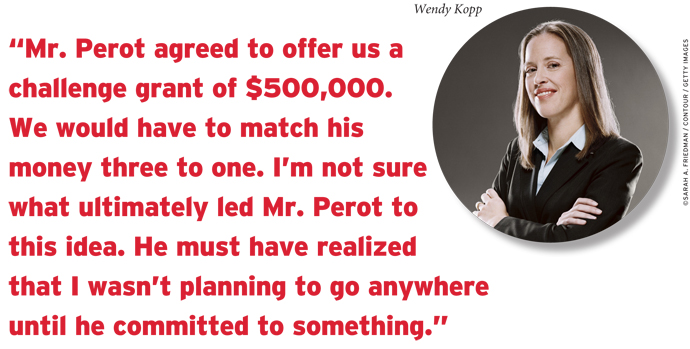

Kopp has described sitting down with Texas billionaire and former presidential candidate Ross Perot, trying to get that $2.5 million:

All I remember is Mr. Perot talking. He talked a lot, and I had trouble following much of what he was saying. I was mostly just thinking ‘I need to stay here until I get $1 million from this man.’ When Mr. Perot suggested that I contact Sam Walton and other philanthropists instead, I insisted that he himself was the best possible prospect. Finally, after two hours of back and forth, Mr. Perot agreed to offer us a challenge grant of $500,000. We would have to match his money three to one. I’m not sure what ultimately led Mr. Perot to this idea. He must have realized that I wasn’t planning to go anywhere until he committed to something.

Kopp remembers that Perot’s grant was “the catalyst we needed,” with other donors following his lead and supplying the remaining funds “in relatively short order.”

Only the most hard-headed or selfless of entrepreneurs muscle through. Those with less stomach for frustration, as well as those interested in doing well in addition to doing good, will steer their energies elsewhere. It’s not just about dollars, though. The impact of venture capital in entrepreneurial hotbeds like Silicon Valley is also a product of the personal networks, mentoring, and expertise that come with it. These networks help new enterprises get a foot in the door, and mentors provide assistance with mundane, but crucial, tasks like organizational bookkeeping, strategic planning, and governance.

Equally crucial is the quality control implicit in venture funding. Those who worry that greenfield efforts may not be publicly run, or who are hesitant to give funds to new ventures with unproven quality, often overlook the fact that competition for venture funding in the private sector comes with intensive screening. In a community like Silicon Valley, as a general rule only 10 percent of business plans that venture capitalists receive warrant any response at all, and only 1 percent are ever funded. To be sure, venture investment also has its share of blemishes. During the late-1990s dot-com bubble, for instance, investors frequently left their skepticism behind as they flocked to a slew of dubious ventures. So, it is not that this process is flawless, but only that it tends to exert a healthy discipline overall.

A particular challenge for schooling is that venture capital is not geographically dispersed. While schools operate in every corner of the country, venture capital is highly concentrated. In 2006, one-third of all venture capital investments were made in California’s Silicon Valley. That figure increases to about half of all investments if Los Angeles, Orange County, and San Diego are included, and to three-fourths of all U.S. venture investment if one adds the Route 128 corridor outside Boston, New York, and metropolitan Washington, DC. In other words, about three-fourths of all investment is made in a few California locales and in the Boston–New York–Washington nexus. Given this natural dynamic, we cannot expect 15,000 school districts to become hotbeds of educational entrepreneurship. Instead, the expectation should be that the requisite funding, infrastructure, and networks will likely emerge in some limited number of locales. Greenfielders need to invest in and build these hubs, and then take care to encourage and support the ventures that are able and willing to deliver their services more broadly.

The quality control and support that the investment process provides are driven by investors tending to their self-interest and happen naturally and invisibly in places like Silicon Valley. They impose a certain flexible but hardnosed quality control even while creating an entire ecosystem and equipping promising new ventures to take root. For too long, these quality assurances and development processes have been overlooked by both K–12 reformers who wonder why innovations fizzle and school choice enthusiasts who seemingly expect manicured flowers to spring from a barren, rubble-strewn plain.

The Three Phases of Investment

The Three Phases of Investment

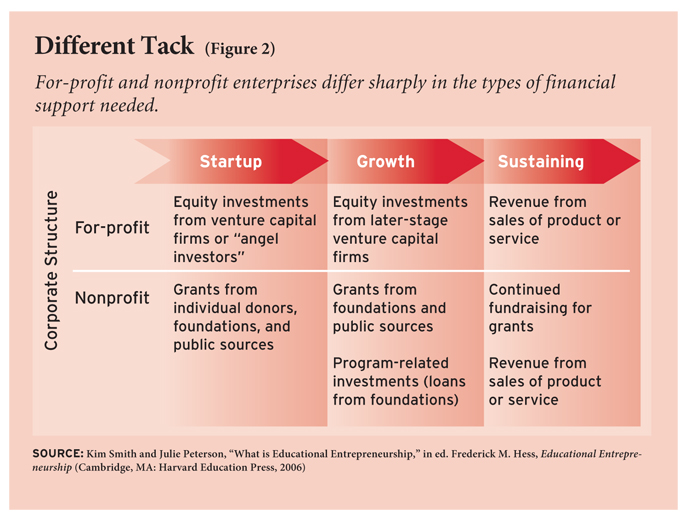

Though all education entrepreneurs need financing to get off the ground (venture capital) and to support expansion (growth capital), the capital market for for-profit organizations is markedly different from the one that nonprofit organizations can access (see Figure 2). While for-profit ventures can theoretically rely on their profits, nonprofits rely on a continuous funding stream (sustaining capital) even once they mature.

Startup Capital

Education entrepreneurs creating for-profit enterprises traditionally raise their initial capital from individuals (“angel investors”) or venture capital firms. As explained in the sidebar, these investors put up cash in exchange for an ownership stake (“equity”) in the new organization, and they expect that their investment will eventually yield a profit.

In 2004, just over $50 million was privately invested in businesses addressing the Pre-K–12 sector. With success stories like Amazon, Apple, and Google, one might think that early venture investors typically do quite well for themselves. But the reality is much more complex. In Fool’s Gold, Scott Shane, a professor of entrepreneurial studies at Case Western Reserve University, argues that observers focus on fabulously successful entrepreneurs, but what they do not realize is that these success stories are incredibly rare. Only a small number of entrepreneurs are really, really successful—and, by extension, only a small number of venture investors see large returns. The media contribute to this misperception because it is easy to tell the story of Google and of early Google investors, but it is much less interesting and more difficult to write stories about failure.

Nonprofit education entrepreneurs generally raise their startup capital from venture philanthropy firms like NewSchools Venture Fund and the Charter School Growth Fund, or from individual donors and foundations. Only a few foundations are comfortable with taking a risk on entrepreneurial education organizations. Those that do make these early funds available—usually multimillion-dollar grants over the course of several years—tend to be younger foundations, like the Eli & Edythe Broad Foundation, the Milton Friedman Foundation, the Michael and Susan Dell Foundation, and the Bill & Melinda Gates Foundation, that have embraced the modern school of venture philanthropy.

Before the relatively recent emergence of these new foundations, funders tended to provide these early grants in only small increments, forcing entrepreneurs to spend enormous amounts of time and energy on fundraising from multiple donors. In addition, foundation officials found it far more palatable to support a host of small, capacity-building grants than to make concentrated bets on greenfield ventures. Foundation officials rarely get in trouble for failing to have an impact, but can quickly get into hot water for supporting politically contentious measures. For this reason, traditional funders have historically preferred to support professional development, curricular reforms, mentoring programs, and similar efforts that are broadly popular and appear to be risk-free.

What Is Venture Capital?

Crucial money for greenfield ventures is startup funding—the kind of investments that are often referred to in business magazines or popular culture as “venture capital.” Venture capital plays a key role in launching and supporting the firms responsible for innovation and growth in the U.S. economy.

Companies backed by venture capital include many of today’s titans, like Intel, Microsoft, Medtronic, Apple, Google, Genentech, Starbucks, Whole Foods, and eBay. In 2007 and 2008, the National Venture Capital Association reports that there were more than 2,400 venture capital deals worth more than $13 billion in the United States, with the bulk of activity concentrated in knowledge-driven industries like software, biotechnology, medical devices, and energy. One would normally expect to see education comfortably ensconced on a list like that—yet it is nowhere in sight.

Since such funding is largely alien to most individuals involved in K–12 education, it is worth taking a moment to understand how venture capital typically works. What exactly is a venture capital fund? It is typically an investment fund initiated by a group of partners who contribute their own money and then raise additional dollars from outside investors. The partnership agreement specifies both the lifespan of the fund (typically 10 years) and the management fee. As Joe Keeney and Daniel Pianko have explained [in Hess, The Future of Education Entrepreneurship], “The typical management fee structure is ‘two and twenty’—that is, 2 percent per year of the total capital raised, plus 20 percent of the profits after…100 percent of their invested capital [has been recovered] at the end of the fund’s life.” Over those 10 years, venture firms raise funds, pursue promising investments, and eventually exit by selling their stakes.

Given the risks, venture capital investors seek to win big or cut their losses. For this reason, they typically provide only enough funding for a venture to reach the next stage of development, so that it can attract support from those with a smaller tolerance for risk. This need to realize investment returns leads new ventures to focus on becoming successful enough to attract buyers, which involves a private transaction or “going public” and selling shares of stock. And a venture capitalist’s aim—to win big on the front end and get out fast once the profit is made—leads venture firms to identify an exit strategy early on.

Growth Capital

For an education entrepreneur, finding startup capital is challenging, but fundraising for growth can be even tougher. For-profit companies that have a good track record may find that venture capital firms such as Quad Ventures are willing to invest in growth for later-stage education organizations with promising early results. Even venture capital firms that don’t focus on education are willing to entertain the notion if they see a successful business emerging.

Nonprofits, on the other hand, have a much more difficult time attracting growth funds. They struggle to raise the kind of large, multiyear investments needed to support expansion because even terrific nonprofit ventures cannot deliver a handsome return to investors. In addition, there is a perverse incentive for growing nonprofit organizations: The better the organization is doing, the more likely donors are to drop their support, believing they have done their part or are no longer needed. As such, many foundations seem willing to support strong nonprofit organizations and help them expand on a limited scale, but few are willing to sustain an organization as it grows over time.

It is especially difficult to raise large amounts of funding from foundations because, according to federal regulations, program officers need only spend 5 percent of the foundation’s total assets each year in the form of grants and other expenses. Except in unusual cases, the other 95 percent of a foundation’s assets are not used to fund grantees but instead are invested for the long term to preserve its endowment. If foundations are to seek a bigger impact, they may need to tap these endowments more aggressively.

One possible strategy for augmenting the available funding relies on program-related investments, which are loans that come from endowment funds. Several foundations, including the Walton Family Foundation and the Annie E. Casey Foundation, have made program-related investments to help charter school entrepreneurs secure facilities for their schools. There is room for more such investment: According to the Foundation Center, foundations nationwide hold nearly $500 billion in their endowments, but use just over $200 million of that for charitable loans or program-related investments—less than one-twentieth of 1 percent.

Nonprofits and philanthropies that have taken on the explicit mission of helping other nonprofits grow include the Growth Philanthropy Network, the Draper Richards Foundation, the Robin Hood Foundation, and the Tipping Point Community. The Draper Richards Foundation, for instance, was founded by famed venture capitalist Bill Draper and seeks to give nonprofits both management knowledge (a Draper Richards board member sits on participating nonprofits’ boards) and capital in their infant stages ($100,000 per year for three years).

Another foundation that is doing things differently is SeaChange Capital Partners, which makes multimillion-dollar infusions to help established nonprofits grow. SeaChange was founded by Chuck Harris, a retired Goldman Sachs partner. Harris had previously worked with nonprofit organizations and noted a serious problem. He explains [in Philanthropy News Daily]:

I was involved with a couple of non-profit organizations that had fantastic management, good results, a fair amount of financial discipline, and were ambitious. And if they had been for-profit businesses at a similar stage of development, they would have gone out and raised a multi-million-dollar, multi-year round of funding tied to their business plan. Instead, they were sending out scattershot proposals for relatively small amounts of money over short periods of time. In other words, there was no financial certainty…[and] the most senior people in the organization were spending a disproportionate amount of their time fundraising as opposed to driving the ship. It seemed to me to be a very ad hoc, inefficient, and restrictive way to grow.

SeaChange adopts Wall Street methods to support proven nonprofits with ambitious growth plans. Harris explains the key shift is “seek[ing] to fund the business plans of these nonprofits rather than [to] fund a piece of their program…. We plan to conduct the financing much like a private placement in the business sector, with the goal of raising $5 million, $10 million, $15 million for organizations on the threshold of a growth phase.”

Scrambling for Startup Capital

Eric Adler is cofounder and managing director of the SEED Foundation, a grades 7–12 boarding school in Washington, DC, that has won awards from Harvard University’s Kennedy School of Government and other entities for its astonishing success sending at-risk kids to college. Adler relates how he and cofounder Rajiv Vinnakota struggled to find funding for the initial DC boarding school. At first, Adler explains, “We thought we were going to build a private school.”

After a quick survey of boarding program costs and what it would require in terms of annual funding or raising an endowment, however, Adler and his partner concluded that “it was not economically feasible. We would have been talking about many hundreds of millions of dollars of endowment. Or it would have meant raising money hand-to-mouth year after year.” Instead, Adler and Vinnakota began looking at nonprofit models in which the government might provide startup capital and then SEED would raise money annually to sustain the school. “You get the slug up front because everyone needs some activation energy and some capital to get going and then after that you raise the money year after year,” Adler explains. But, he adds, “We…pretty quickly concluded that that wasn’t going to work, either. Because, again, it was going to involve a level of annual fundraising that just wasn’t sustainable.”

After dismissing those two stratagies, Adler wondered, “Could [we] reverse it? Could [we] go to the private sector and get the upfront slug of money in exchange for getting the public sector to promise the operating costs indefinitely?” This led the SEED Foundation to charter schooling. Adler recalls Vinnakota and himself approaching DC and federal officials and saying, “In exchange for the private sector putting up a whole bunch of new facility money, would you be willing, then, to pay the difference between the regular day cost and the boarding cost?” And they were talking simultaneously to philanthropists and private-sector investors, saying, “Yes, we need to raise a bunch of money from you now, and we’ll still have to raise some in the first few years while we’re getting up to scale. But once we get up to scale, we promise we’ll never come back to you saying we won’t survive unless [you’re willing to provide additional support].” This strategy allowed the SEED Foundation to raise the required $25 million for the 1999–2003 launch of the school.

Sustaining Capital

Entrepreneurial K–12 ventures launch and grow with private capital or philanthropic support. Once up and running, however, sustainable ventures seek to rely on earned income from fees or the sale of products or services. However, despite increasing acceptance of income-generating for-profit and nonprofit organizations, few education entrepreneurs have built models that sustain themselves on these revenues alone. And, as Dan Katzir and Wendy Hassett of the Eli & Edythe Broad Foundation have observed [in Hess, With the Best of Intentions], “Many foundations will not support a grantee for more than a specified number of years, regardless of where the organization is in terms of its growth cycle.” This means that nonprofits scramble to offset the loss of philanthropic support by finding ways to sell their services or by finding new funders, while for-profits seek to achieve a scale that makes them economically viable. One of the few successful school builders to have addressed this challenge is National Heritage Academies, a for-profit charter operator that enrolls 35,000 students in 57 schools across 6 states and has managed to attain profitability while generating impressive academic outcomes. Even academically successful ventures, however, have found it challenging to mimic NHA’s financial success.

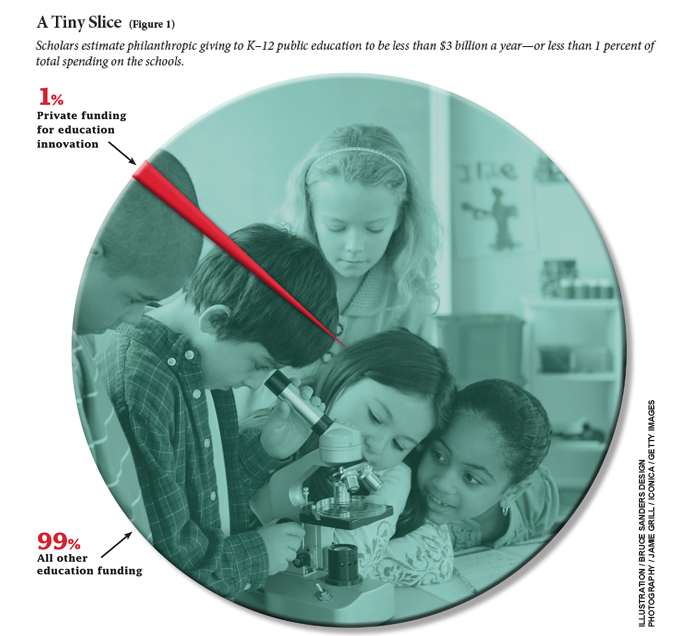

Although some nonprofit education entrepreneurs can support their organization’s ongoing operations through public funding—such as by per-pupil dollars that flow to charter management organizations—most rely, at least in part, on fundraising from individuals and foundations. The limits to this approach are legion, however, as scholars estimate that total philanthropy to K–12 probably amounts to less than $3 billion a year—or less than 1 percent of all K–12 spending [as shown in Figure 1]. To date, entrepreneurial ventures have been disproportionately funded by this tiny sliver of funding—and especially by funds from younger foundations with roots in the 21st-century economy.

Some leading “new” philanthropies, like the Gates, Walton, and Broad Foundations, have attempted to adapt the venture investment mind-set to the social sector. Funders have begun to weigh criteria like scalability and financial sustainability more heavily, have taken seats on nonprofit boards, and have requested regular performance updates. This marks a shift in thinking—though it’s a development that has also encountered skepticism as to how willing these funders actually are to take bold chances and whether their efforts sometimes cross from smart oversight into micromanagement. Whatever one makes of such concerns, it is clear that support from philanthropic funders has proven instrumental in launching or expanding heralded greenfield ventures like KIPP, New Leaders for NewSchools, Aspire Public Schools, College Summit, Green Dot, and Achievement First.

In education circles, the two best-known venture philanthropies may be the decade-old NewSchools Venture Fund and the much younger Charter School Growth Fund. The San Francisco-based NewSchools Venture Fund secures investments from both for-profit and nonprofit sources and then seeks to provide startup capital to ventures—both nonprofit and for-profit organizations—that are sustainable and designed to achieve scale. The Colorado-based Charter School Growth Fund, with over $150 million in support, provides grants and loans to promote the growth of high-quality charter management and support organizations. These venture philanthropists accept that some investments will fail, so long as the failures are the product of efforts to address hard, important challenges. As the Broad Foundation’s Katzir and Hassett have explained, “We do not regard our grantmaking as charity…[but] think of our work as making investments in areas in which we expect a healthy return.”

This article appeared in the Summer 2010 issue of Education Next. Suggested citation format:

Hess, F.M. (2010). Fueling the Engine: Smarter, better ways to fund education innovators. Education Next, 10(3), 30-37.