Proposals to make college free and forgive student debt have been criticized for disproportionately delivering benefits to high-income families. This pattern is difficult to reverse because students from high-income families are more likely to attain higher levels of education and to borrow more for college and graduate school. And it means policymakers seeking to forgive large amounts of debt face a trade-off between generosity and targeting.

This analysis examines how different approaches to loan forgiveness, including plans put forward by members of Congress and presidential hopefuls, would distribute benefits to Americans of different income levels and races and ethnicities.

On Monday, democratic presidential candidate Julián Castro released his education platform, which includes targeted loan forgiveness for student debt holders who also receive benefits through means-tested federal assistant programs. Former Rep. Jared Polis (D-CO) proposed canceling all student debt last year, and last month Sen. Elizabeth Warren (D-MA) proposed forgiving up to $50,000 of debt for individuals in households with annual incomes of up to $100,000, with progressively smaller amounts of forgiveness for families making up to $250,000 a year.

I analyzed data on federal student debt from the 2016 Survey of Consumer Finances, using the same methodology as a previous Urban Institute analysis of Warren’s debt cancellation plan.

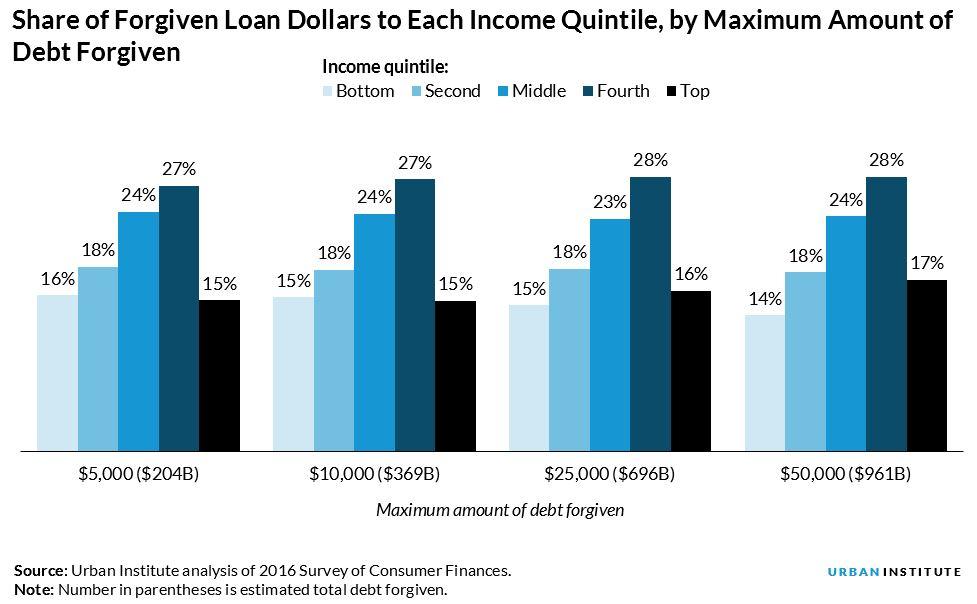

Reducing the maximum amount of debt forgiven

Households with higher incomes tend to have more student loan debt. So, forgiving larger amounts of debt would distribute a larger share of benefits to higher-income households, and reducing the amount of debt forgiven should increase the share of benefits going to lower-income households.

Looking at the Warren plan, reducing the maximum amount of debt forgiven would slightly increase the share of benefits going to low-income households. Reducing the amount of debt forgiven dramatically decreases the total amount of loans forgiven, from an estimated $961 billion at $50,000 of forgiveness to $204 billion at $5,000 of forgiveness. Thus, the total amount of dollars going to all income groups decreases as the plan gets less generous, even if the percentage of dollars only slightly changes.

Under the most generous plan (up to $50,000), the lowest-income families would get 14 percent of the benefits, or about $135 billion. Under the least generous plan ($5,000), the same group would get 16 percent of the benefits, or about $33 billion.

Changing eligibility rules for debt forgiveness

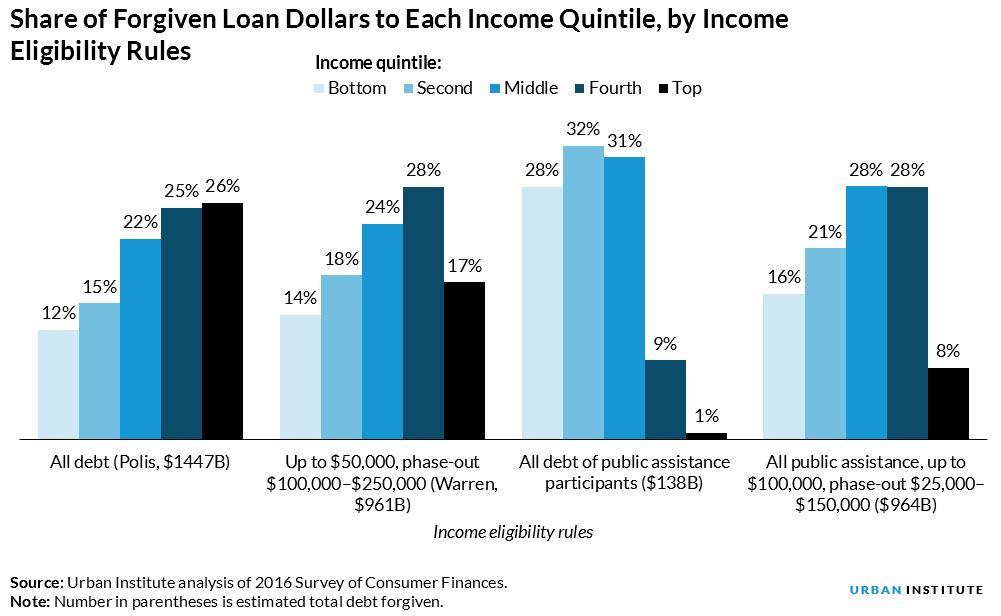

The Warren plan would provide benefits to families making up to $250,000, or about 98 percent of households with debt. The $50,000 forgiveness limit would be gradually reduced starting at $100,000 of income; for example, a borrower with a household income of $200,000 would be eligible for up to about $17,000 of forgiveness.

Compared with the Polis proposal to cancel all federal student loans, Warren’s income-based targeting reduces the total amount of loans forgiven by about one-third, significantly reduces the share of benefits going to the highest-income families, and modestly increases the share of benefits going to low-income groups.

An alternative approach would be to use participation in means-tested federal benefit programs, such as Temporary Assistance for Needy Families (TANF), as a proxy for economic hardship, rather than household income. Castro’s proposal would offer partial loan forgiveness for people who have received means-tested assistance for three years over a five-year period.

About 16 percent of households with debt receive benefits from the Supplemental Nutrition Assistance Program (SNAP), TANF, or another public assistance program, which is likely an underestimate because of underreporting of program participation in survey datasets. The share of borrowers participating in these programs decreases from 37 percent among families in the bottom income quintile to 17 percent of middle-income families to less than 1 percent of the highest-income families. Eligibility rules for programs such as SNAP consider family size, which can make middle-income families eligible, and assets, which can make low-income, high-asset families ineligible.

Forgiving all education debt for households that participate in public assistance programs would concentrate benefits on low- and middle-income Americans, with the majority of forgiven dollars (60 percent) going to people in the bottom two income quintiles. About $138 billion in loans would be forgiven.

This kind of plan could be combined with a Warren-style plan. I simulate the benefits of such a plan that forgives all federal loans of public assistance participants and up to $100,000 of the loans of families making up to $25,000, with lower amounts of forgiveness for families making up to $150,000.

This hypothetical plan forgives approximately the same total amount of loans as Warren’s proposal but distributes a somewhat greater share of benefits to low-income families (16 versus 14 percent for the bottom quintile) and a significantly lower share to the highest-income families (8 versus 17 percent).

Estimated loan forgiveness by race and ethnicity

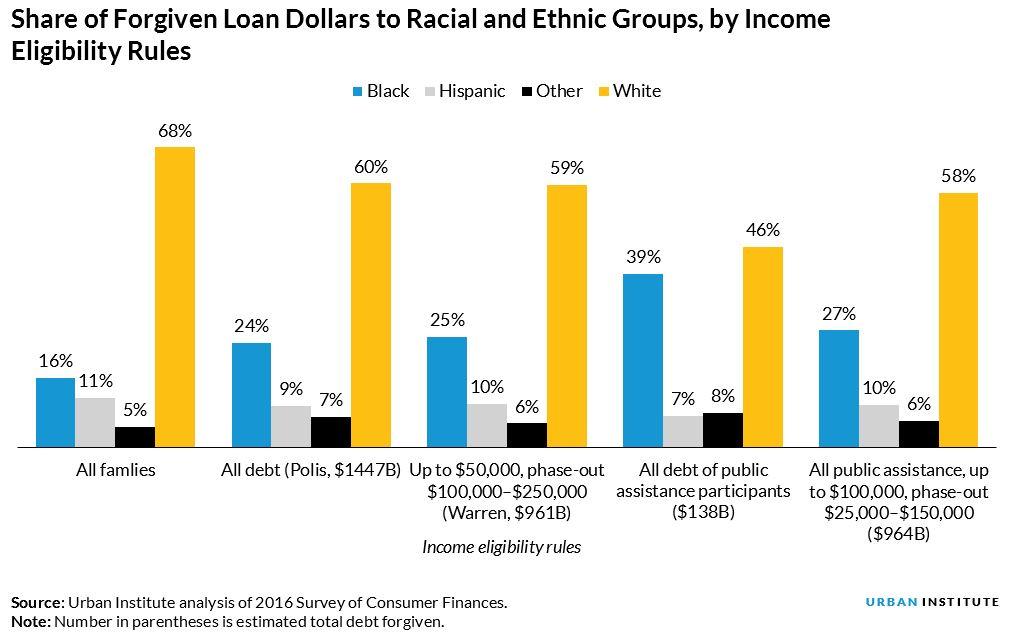

Projecting the distribution of debt forgiveness by income only tells part of the story, given the close connection between student borrowing and the racial wealth gap.

Among the options considered in my analysis, providing full loan forgiveness to recipients of public assistance would direct the largest share of benefits to black Americans (who make up 16 percent of all households)—about 39 percent, compared with 25 percent under Warren’s plan. But Warren’s plan is more generous overall and would forgive about $240 billion of black families’ debt, compared with $54 billion under a plan limited to public assistance recipients.

Combining full forgiveness for public assistance participants with up to $100,000 in forgiveness for other low-income households would direct the greatest number of dollars to black families—$260 billion, or about 27 percent of all forgiven loan dollars.

The fact that even targeted loan forgiveness programs provide significant benefits to economically well-off families highlights the constraints policymakers face in seeking to forgive large amounts of student debt. Providing a generous benefit to low-income families and avoiding cliff effects often leads to significant benefits for higher-income families.

One way to approach this problem would be to consider several years of borrowers’ incomes when deciding how much debt to forgive. For existing borrowers, it might mean identifying families that have had low incomes (or who have participated in public assistance programs like SNAP or TANF) for multiple years. For new borrowers going forward, it might involve making income-driven repayment universal and automatic. Estimating the costs and benefits of these kinds of plans is difficult but is critical to designing student loan reforms that are efficient and equitable.

Matthew M. Chingos is a Senior Fellow at the Urban Institute.

This post originally appeared on Urban Wire.