Elementary and secondary private school tuition is a significant investment for many families. And private school leaders, who see the children from these families every day and know the parents in their school community, recognize families’ sacrifices.

“There is a desire from a lot of families that are doing everything they can to afford a private education for their children, and financially they are under a lot of pressure to make that happen,” says Dr. Marc Stout, head of Gaston Christian School in North Carolina.

“They will work second jobs, third jobs whatever it takes. Parents will sacrifice and forgo other things,” says Stout.

More than half of U.S. states provide families with private learning options, from scholarships to education savings accounts, to help students from all walks of life find an effective education. While state policymakers should be leading these efforts, Washington’s move to expand the uses of college savings plans to include K-12 private school tuition in last year’s Tax Cuts and Jobs Act (TCJA) gives families more options with their own savings for their child’s future.

According to federal law, families can save money in 529 savings accounts (named after section 529 of the Internal Revenue Code) and use their savings for K-12 tuition or college tuition and expenses. Account holders can use the savings without paying federal taxes on the growth of the investments. Many states also offer tax incentives to account holders. Some 12.5 million 529 accounts are open in the U.S., totaling more than $304 billion in assets, according to the Investment Company Institute.

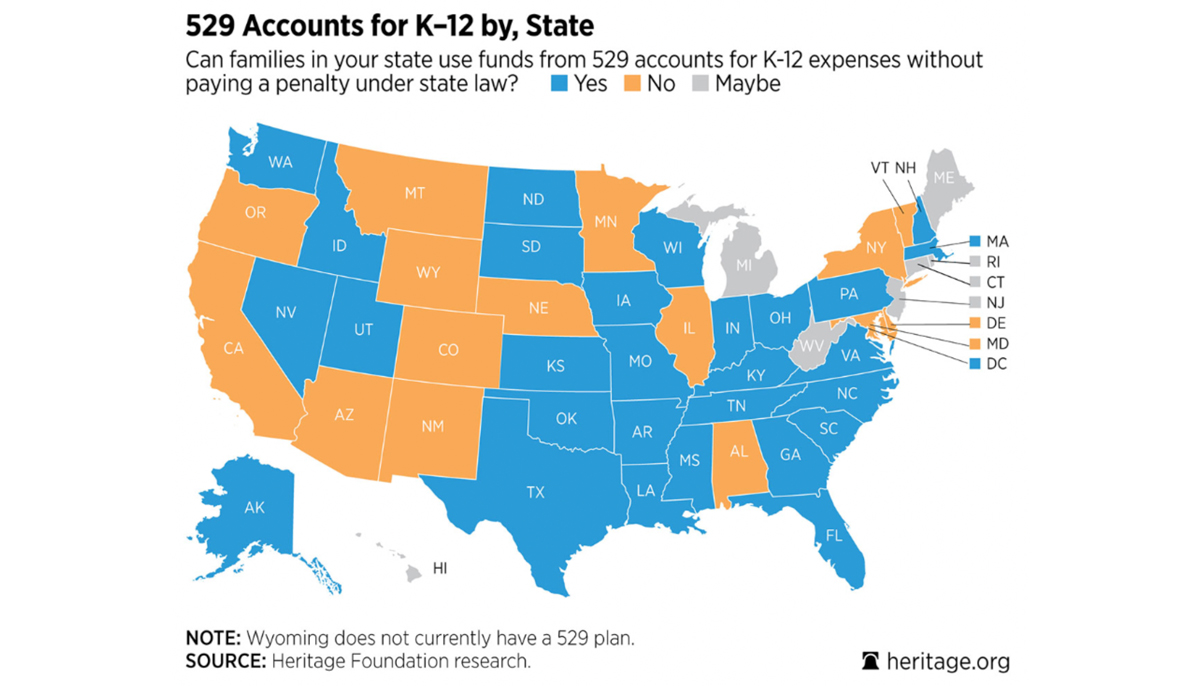

But just because Washington changed federal law doesn’t mean every state’s law conforms with the changes. After the president signed the TCJA, state officials began investigating whether their laws governing college savings plans conflicts with federal statute. For months last year, state treasurers and 529 investment providers posted messages on their web sites saying the implications of the new changes were under review.

As of the end of 2018, just over half of U.S. states have statutory provisions that allow the use of 529 savings plans for K-12 private school tuition. For example, Mississippi’s statute says that any education expense in section 529 of federal law is allowed, and Mississippi’s state treasurer posted a letter confirming this for state taxpayers. Louisiana officials had to enact new legislation to allow state families to use their accounts for K-12 private schools. Oregon lawmakers are using legislation to prevent families from taking advantage of the new option.

Now that the election results are in, some states have new officials overseeing 529 savings plans, which could mean more changes when state legislative sessions begin later this month.

To help make sense of what is happening state-to-state, a new Heritage Foundation resource explains which states have ambiguity in their laws regarding 529 plans and K-12 private school tuition and those states that clearly allow families the new option. (The site will be updated throughout the year.)

In some states, 529 investment plans and even state agencies have said that state taxpayers can use their savings for K-12 tuition, yet state code remains unchanged—often referencing only higher education expenses. State lawmakers should use next session to clear up this ambiguity. Families would have the most opportunity afforded to them if state code said that state taxpayers can use their 529 college savings plan for any qualifying education (not just “postsecondary education”) expenses in federal law, as amended.

Some argue that families won’t have enough time to realize growth in a 529 plan even if they create an account when their child is born. But no one is forcing families to use 529 savings for K-12 tuition, and the decision about how best to provide quality learning opportunities should be left to parents and families.

“I think the 529 helps families make their dollars go further,” Stout says. “The 529 is a student-centric and parent-centric move.”

The size of these college savings plans depends on how much a family is able to put away for the future—and these parents should be able to choose how to use their own savings to help their child succeed.

— Jonathan Butcher

Jonathan Butcher is a senior policy analyst in the Center for Education Policy at The Heritage Foundation.