Executive Summary

The moment they earn their bachelor’s degrees, black college graduates owe $7,400 more on average than their white peers ($23,400 versus $16,000, including non-borrowers in the averages). But over the next few years, the black-white debt gap more than triples to a whopping $25,000. Differences in interest accrual and graduate school borrowing lead to black graduates holding nearly $53,000 in student loan debt four years after graduation—almost twice as much as their white counterparts. While previous work has documented racial disparities in student borrowing, delinquencies, and defaults, in this report we provide new evidence that racial gaps in total debt are far larger than even recent reports have recognized, far larger now than in the past, and correlated with troubling trends in the economy and in the for-profit sector. We conclude with a discussion of policy implications.

Amidst the general public concern over rising levels of student loan debt, racial disparities have attracted increasing attention. In 2006, a U.S. Department of Education report noted that black graduates were more likely to take on student debt, and in 2007, an Education Sector analysis of the same data found that black graduates from the 1992-93 cohort defaulted at a rate five times higher than that of white or Asian students in the 10 years after graduation (Hispanic/Latino graduates showed a similar, but somewhat smaller disparity).[i] Recently, momentum on the topic has been growing, with several new studies documenting how students of color are disproportionately burdened by student debt:

• A 2014 study by Goldrick-Rab, Kelchen, and Houle and a 2015 report by Demos show that black students borrow more than other students for the same degrees, and black borrowers are more likely than white borrowers to drop out without receiving a degree.[ii]

• A creative 2016 analysis by the Washington Center for Equitable Growth matched data on student loan delinquencies by zip code with zip code demographics and finds that delinquencies are concentrated in black and Latino communities.[iii]

• Two recently published studies (by Addo, Houle, and Simon and Grinstein-Weiss et al.) use national survey data to show that black students hold substantially more debt by age 25 compared to their white counterparts, and that disparities are evident even after controlling for family income and wealth, indicating that differences in postsecondary and labor market experiences contribute to the debt gap.[iv]

Unfortunately, because the U.S. Department of Education does not regularly track borrowers by race, data limitations have hampered efforts to connect research on racial gaps with detailed new studies of debt and default patterns. For example, highly-cited recent research which analyzed administrative data linking borrowers, future earnings, and defaults cannot be broken out by race.[v] Information on race is not collected on the Free Application for Federal Student Aid (FAFSA), nor is it included in the National Student Loan Data System (NSLDS) which tracks outstanding debt and repayments. Most of what we know about the debt gap is based on cross-sectional surveys conducted by the U.S. Department of Education only once every four years, which don’t allow borrowers to be tracked over time, or on longitudinal surveys which are conducted even less frequently.

In August 2016, the National Consumer Law Center (NCLC)—supported by nearly 40 other public interest groups, including the American Civil Liberties Union (ACLU)—sent a letter to Education Secretary John King demanding the department track and remedy the disproportionate consequences of student loan debt for borrowers of color.[vi] “For nearly a decade,” the letter states, “the Department of Education has known that student debt impacts borrowers of color differently from white borrowers. Yet in that decade, the Department has failed to take sufficient steps to ameliorate the disproportionately negative impact on borrowers of color, or even to conduct further research to discover the causes or the extent of disparities.”

As we will show, this concern is well-justified. Cross-sectional analyses which do not follow borrowers over time, as well as longitudinal analyses that track graduates from distant cohorts and/or rely upon self-reported debt amounts (which are known to be underreported[vii] and generally inaccurate[viii]), can lead to dramatic understatements of racial disparities in student loan debt.

In this report, we present new analyses of restricted-use data from the Department of Education’s Baccalaureate and Beyond (B&B) 93/97 and 08/12 surveys, which follow graduates from the 1993 and 2008 cohorts through 1997 and 2012, respectively. We supplement with additional Department of Education and Census Bureau data, in order to document the vast racial disparity in student debt, explore possible causes, and discuss policy implications. Importantly, the B&B surveys are linked to administrative NSLDS data on student loan borrowing, repayment, and default rather than relying on self-reports. The B&B:08/12 does not yet follow students as long as its 1993 counterpart (which ultimately followed students for 10 years post-graduation), but already provides sufficient follow-up to reveal distressing racial disparities.

We find that previously-reported differences in debt at graduation—of about $7,400—are less than one-third of the total black-white debt gap four years later, due to differences in both repayments and new graduate borrowing (we focus primarily on the black-white gap, which is by far the most pronounced). Four years after graduation, black graduates have nearly $25,000 more student loan debt than white graduates: $52,726 on average, compared to $28,006 for the typical white graduate.[ix] Despite reductions in default rates between the 1992-93 and 2007-08 cohorts, black college graduates are still substantially more likely to default on their debt within four years of graduation (7.6 percent versus 2.4 percent of white graduates). And nearly half of black graduates (48 percent) owe more on their federal undergraduate loans after four years than they did at graduation, compared to just 17 percent of white graduates (a situation known as negative amortization).

Our analysis reveals the surprising, disproportionate role of graduate school enrollment—particularly for-profit graduate enrollment—in contributing to the overall black-white debt gap, and raises questions about how these racial debt disparities will further evolve beyond the end of the follow-up period. Unfortunately, these questions will remain unanswerable until we have better ways of tracking student debt by race over a longer period of time. Below, we highlight our main findings and conclude with a discussion of policy implications.

Finding #1: Racial disparities in student debt are larger than previously understood, and have grown dramatically in recent decades.

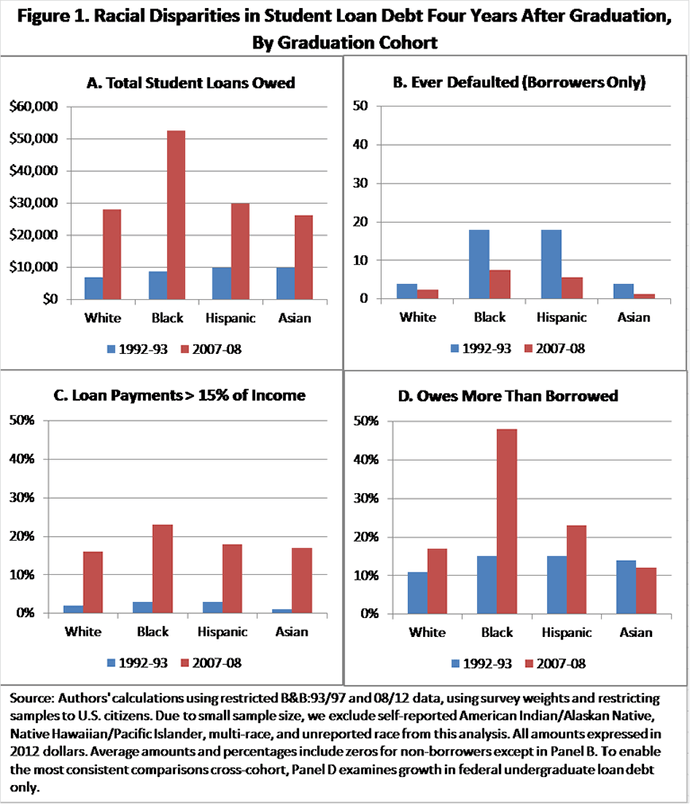

Four years after earning a bachelor’s degree, black graduates in the 2008 cohort held $24,720 more student loan debt than white graduates ($52,726 versus $28,006), on average.[x] In the 1993 cohort, the difference was less than $2,000 ($8,723 versus $6,917; amounts adjusted to 2012 dollars). Figure 1, Panel A below shows that Hispanic and Asian graduates have debt burdens much more similar to white students.

What are the consequences of these large disparities in debt? Default rates among borrowers have actually fallen sharply among all races (see Figure 1, Panel B), likely due to changes throughout the 1990s which increased the penalties for institutions with high default rates and made it harder for students to avoid making repayments even after entering default (more recently, new repayment options may also have played a role).[xi] Still, black borrowers remain more than three times as likely to default within four years as white borrowers (7.6 percent versus 2.4 percent). Hispanic borrowers, despite having about the same level of debt as white graduates, are more than twice as likely to default (5.7 percent).

Moreover, just because borrowers have not defaulted within four years does not mean they are out of the woods. The income-contingent repayment, forbearance, and deferment provisions that help protect students against the worst outcome of default may also obscure other signs of borrower distress: for example, nearly half (48 percent) of all black graduates owemore on their federal undergraduate loans at this point than they did at graduation, compared to just 17 percent of white graduates (Figure 1, Panel D).

Finding #2: Differences in undergraduate borrowing explain less than a third of the black-white gap in total debt four years after graduation.

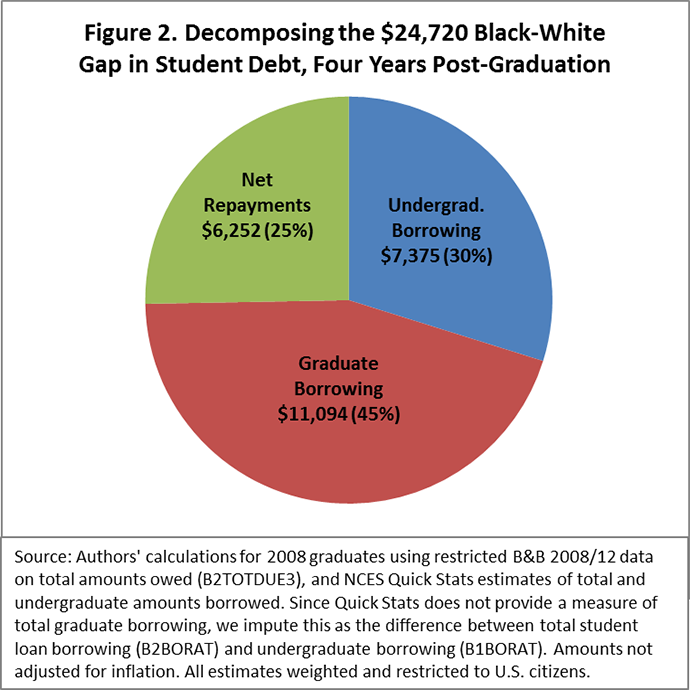

At graduation, black students owe $7,375 more than their white peers ($23,420 versus $16,046). This difference represents less than a third (30 percent) of the nearly $25,000 black-white gap in total debt that exists four years later.[xii] For blacks, undergraduate debt at graduation accounts forless than half of total debt owed, compared to 62 percent for white graduates.

A full 45 percent of the black-white gap ($11,094) comes from differences in borrowing for graduate school. Black college graduates are almost twice as likely as white graduates to accumulate graduate school debt (40 percent versus 22 percent). These differences in graduate school borrowing are driven by significantly higher rates of graduate enrollment (discussed more below), as well as higher rates of borrowing conditional on enrollment.

Finally, about one-quarter of the gap in total debt ($6,252) comes from differences in rates of repayment and interest accrual. Black graduates are much more likely to experience negative amortization (interest accumulating faster than payments received): nearly half (48 percent) of black graduates see their undergraduate loan balances grow after graduation, compared to just 17 percent of white graduates. On net, black graduates owe 6 percent more than they have borrowed, while white graduates owe 10 percent less than they have borrowed, four years after graduation. Differences in repayment rates may be partly attributable to growing black-white wage gaps, as well as to differences in graduate enrollment (which allows students to defer loan payments).[xiii]

Finding #3: Graduate school enrollment rates increased substantially for blacks between the 1993 and 2008 cohorts, much more so than for other groups, and the differential growth has occurred almost exclusively in the for-profit sector.

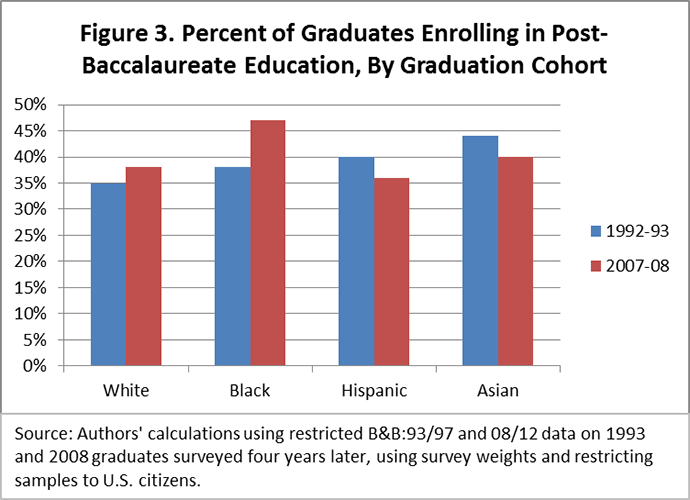

Nearly half of black graduates (47 percent) in the 2008 cohort enrolled in a graduate school degree program within four years, compared to 38 percent of white graduates (see Figure 3).[xiv] This is a shift from 15 years prior, when black graduates were only slightly more likely to enroll in graduate school compared to white graduates (38 percent versus 35 percent).[xv]While this may be a positive trend in general, we also find that among graduate school enrollees, more than a quarter (28 percent) of black graduate students enroll in for-profit institutions—compared to just 9 percent among white graduate students.[xvi]

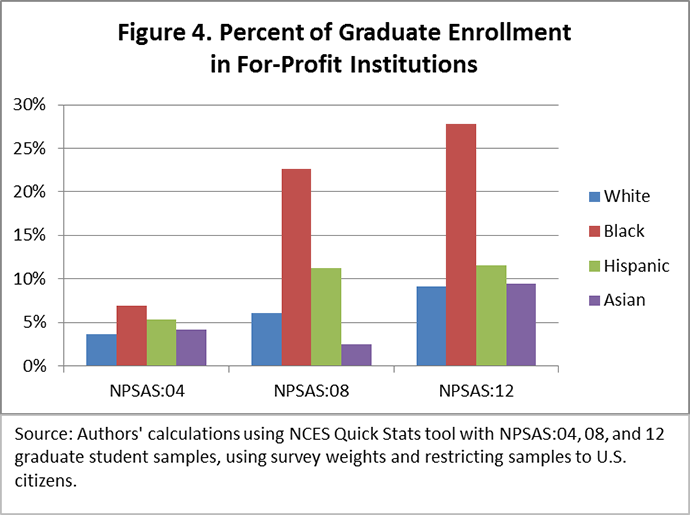

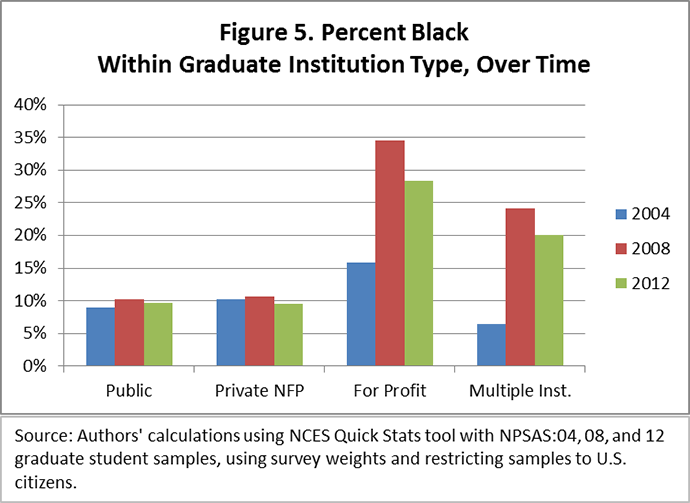

While we cannot separately identify for-profit graduate enrollment for 1993 graduates, cross-sectional enrollment data from the National Postsecondary Student Aid Survey (NPSAS) allow us to examine how graduate enrollment patterns have changed over time. Figure 4 shows that as recently as 2004, for-profit institutions accounted for no more than 7 percent of enrollment among any racial subgroup. But between 2004 and 2008, for-profit graduate enrollment increased dramatically for black students. Indeed, Figure 5 shows that growth in for-profit enrollment (and “multiple institution” enrollment, which may also include some for-profit enrollment) can account for all of the differential growth in black graduate school enrollment between 2004 and 2012: at public and private not-for-profit institutions, black students have remained a roughly constant percentage of the graduate population.

Two factors may contribute to the rapid growth in black graduate enrollment. First, the Higher Education Reconciliation Act of 2005 (HERA 2005) greatly increased federal borrowing limits for graduate students.[xvii]Beginning in 2006, graduate students could borrow up to the cost of attendance via the Grad PLUS loan program; previously, graduate students were limited to the annual Stafford Loan maximum of $20,500. The expansion of graduate loans may have had a differential effect on black graduates, who have less parental wealth to draw upon. And for-profit institutions—where the typical graduate enrollee racks up $33,000 in debt—may have been quickest to respond to the new market opportunity. It’s important to note that graduate enrollment has also increased at public and private not-for-profits, and that graduate students at private not-for-profits accumulate even higher levels of debt.[xviii] But the for-profit sector is by far the fastest-growing sector and the only sector that has seen enrollments grow differentially by race.[xix]

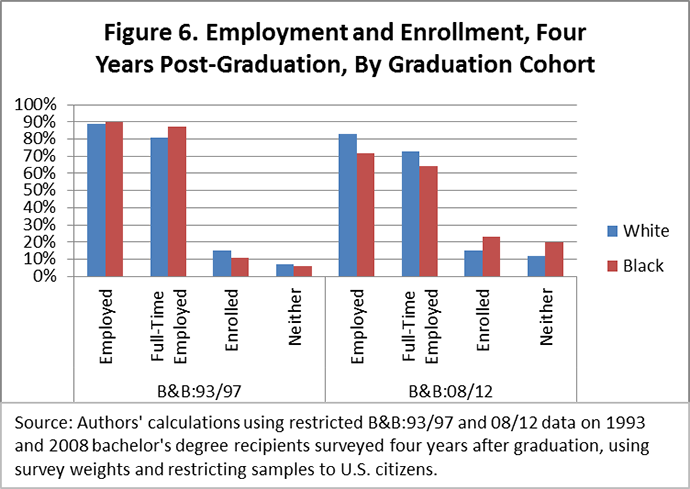

Second, these increases occur alongside evidence of growing racial gaps in college graduates’ labor market outcomes, suggesting graduate school may for some students be a response to the weak post-recession labor market. Among the 1993 cohort, black graduates were just as likely as white graduates to be employed four years later (90 percent versus 89 percent) and slightly more likely to be employed full-time (87 percent versus 81 percent). But among the 2008 cohort—who graduated just on the cusp of the Great Recession—the employment rate drops sharply to 72 percent for black graduates, while dipping more modestly to 83 percent for white graduates (see Figure 6). This employment gap is consistent with other data[xx]showing that the Great Recession hit black college graduates much harder than white college graduates, as well as with evidence[xxi] that employers are more likely to discriminate against minorities in weak labor markets.

Finding #4: The striking black-white disparities we find are far more pronounced than the gaps by parental income or education, and the black-white gap is the only one that grows substantially after graduation.

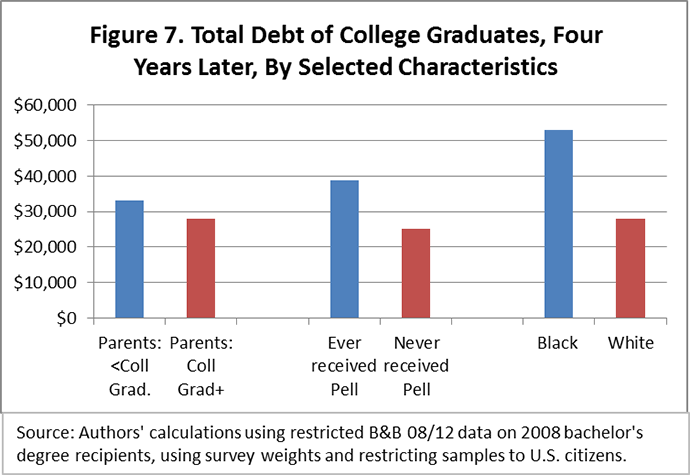

Finally, an important finding of our investigation is that the patterns we report above are largely specific to the black-white debt gap: they cannot be explained away by racial differences in parental education or income. It is certainly true that students from poorer or less-educated families accumulate more debt than those from richer or more highly educated families. But Figure 7 shows that the black-white total debt gap is five times bigger than the debt gap by parental education, and almost twice as big as the debt gap between those who received Pell grants as undergraduates and those who did not.

Moreover, for these other groups the debt gap at graduation is indicative of the debt gap that exists four years later—the black-white gap is the only one that more than triples in size. Unlike the patterns we observe by race, college graduates’ employment rates do not vary substantially by parental education or Pell grant eligibility. And unlike black graduates, first-generation college graduates and Pell-recipient graduates are substantiallyless likely to attend graduate school than their peers.[xxii]

Finding #5: Graduate enrollment is a good investment on average—but for blacks, it entails significantly more financial risk than it does for whites.

To the extent that black-white debt disparities are driven by higher rates of graduate enrollment, is this a problem to solve or a sign of progress to celebrate? Graduate degrees confer large returns in the labor market: graduate degree-holders in 2012 earned 21 percent more than those with only a bachelor’s degree.[xxiii] Analyzing data on 25-45 year olds in the American Community Survey (ACS), we find that the additional earnings boost from graduate degrees is even larger for black students (though our estimates suggest that blacks with graduate degrees still earn less on average than whites with only a bachelor’s degree).[xxiv] Thus, it is possible that higher rates of borrowing in the short term could lead to improved outcomes further in the future.

This optimistic scenario, however, is far from guaranteed, and a number of patterns in the data give cause for concern. First is the disproportionate concentration of black graduate students in the for-profit sector—a sector which, at the undergraduate level, has been riddled with problems concerning high-debt, low-quality, and sometimes even fraudulent programs.[xxv] Unfortunately, the ACS data do not enable us to separately estimate returns by graduate institution type, and the dramatic increase in for-profit enrollments is too recent to have much influence on aggregated estimates from the ACS (which pool across recent and older cohorts).

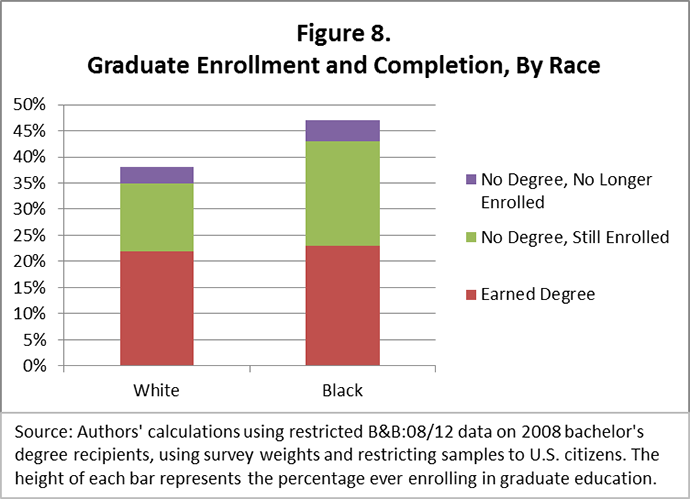

Second, graduate degree completion rates appear to be lower, or at least slower, for black graduate students than white graduate students. As Figure 8 shows, black bachelor’s degree holders are about as likely as their white counterparts to have earned a graduate degree four years later (23 percent versus 22 percent) despite their much higher rates of graduate enrollment.

Third, even if graduate degrees remain a good investment on average, black students clearly face substantially greater financial risk in pursuing them given their higher levels of borrowing and lower average earnings. Using the B&B:08/12 data, we examine total debt-to-income ratios for individuals who are employed full-time in 2012 and not currently enrolled, and find that black students with graduate degrees have debt-to-income ratios that are 27 percentage points higher than white graduate degree holders (even after controlling for other characteristics such as parental education and income).[xxvi] While default rates are still much lower for black borrowers with any graduate enrollment versus no graduate enrollment (3.9 percent versus 12.3 percent), 42 percent of black borrowers with graduate enrollment are still deferring their loan payments, making the default rates less informative regarding long-term repayment prospects.[xxvii]

Discussion and Implications

In their August letter to Secretary King on behalf of 40 public interest groups, the NCLC highlights some of the troubling causes and consequences of racial disparities in student debt, including racial targeting by for-profit institutions and abusive debt collection practices.[xxviii] Our new findings suggest their concern is not only justified, but may well be understated. We conclude with the following policy implications:

Implication #1: In order to truly understand the causes and consequences of massive racial disparities in student debt, we need to be able to track debt and repayment patterns by race.

Being able to track a cohort of bachelor’s degree recipients for four years, once every fifteen years, is helpful, but insufficient. While the B&B:08/12 cohort will be surveyed a final time in 2018, given high rates of graduate school enrollment, even a ten-year follow up may not fully capture the long-term consequences of racial debt disparities. We also need to be able to track the debt gap with greater frequency, as contextual factors—including economic conditions, financial aid policies, and the role of for-profits—can change quickly. The most practical way to do this is to collect information on borrower race so that it can be incorporated into administrative databases that track borrower outcomes.

Incorporating race into administrative databases would also fill the gaping data void regarding how racial debt disparities evolve for those that leave college without a bachelor’s degree (there is no equivalent to the B&B survey at other attainment levels). Recent analyses of administrative data suggest that borrowers who leave college without earning a degree are at even greater risk of default than those who graduate, even if they graduate with more debt. And prior reports have already documented large racial disparities in the likelihood of leaving college without a degree.[xxix] In fact, more than one in every four black college entrants (28 percent) leaves college with debt, but no degree—a precarious status that applies to only 15 percent of white college entrants.[xxx]

Finally, data availability is not the only factor explaining the limited research in this area; researchers also need to pay attention to the data that do exist. Where data allow, any analyses of student debt should be attentive to heterogeneity by race. Where data do not allow, analysts should acknowledge that the patterns that hold for the majority may be very different for borrowers of color.

Implication #2: Research and policy focusing on undergraduate borrowing alone will address only a fraction of overall racial disparities in student debt.

Among college graduates, the black-white gap in undergraduate borrowing is less than a third of the total gap four years later. Our analysis highlights the substantial role of graduate school in expanding the black-white debt gap, and indicates that the enrollment growth for blacks has been highly concentrated in the for-profit sector. We thus need more evidence on the payoffs of specific types of graduate education, particularly in the rapidly-growing for-profit sector. In addition, the financial aid system—which treats all graduate students as independent, and thus does not consider parental income—fails to acknowledge systematic racial and socioeconomic differences in financial support that continue throughout young adulthood.

Our findings also add to prior evidence that differences in labor market outcomes—employment rates and earnings—exacerbate racial debt gaps.[xxxi] If these gaps are evident among college graduates who have generally strong employment prospects, they may be even worse among those who leave college without a bachelor’s degree.

Finally, it is important to recognize that reducing debt by simply discouraging or limiting student borrowing—at either the undergraduate or graduate level—is not a solution, and could well make educational disparities worse.[xxxii] A recent study by Jackson and Reynolds, for example, finds that loans promote higher rates of persistence and completion among black undergraduates, and concludes that despite racial gaps in default rates, loans are nonetheless “an imperfect, but overall positive tool for reducing educational inequality” by race.[xxxiii]

Implication #3: New repayment options such as the Revised Pay-As-You-Earn (REPAYE) plan may alleviate the worst consequences of racial debt disparities, while failing to address underlying causes.

Income-contingent loan repayment options, including the newest and most generous REPAYE plan, adjust borrowers’ monthly payments according to their income and ultimately forgive debts that remain after a set period of repayment. In theory, such plans can help borrowers of any race manage even relatively large amounts of debt. The paperwork burden currently associated with such plans can be daunting, however, and too often students do not learn about income-contingent options until after they are already in trouble—having missed payments, accumulated fees, and damaged their credit. As a solution, some scholars have proposed automatically enrolling borrowers in income-contingent repayment, and administering it via the tax system so that payments adjust immediately and automatically to changes in earnings.[xxxiv]

While income-contingent repayment can help reduce the worst consequences of the racial debt gap, it treats the symptoms without acknowledging or remedying the underlying causes of the disparity. Plans like REPAYE are meant to address the idiosyncratic risks of educational investments—not to address systemic racial inequality resulting from historical discrimination (leading to low parental wealth), ongoing racial bias in the labor market, or predatory recruitment by for-profit institutions. Federal financial aid policy alone cannot solve these problems—but neither can it ignore the challenges facing students of color who disproportionately bear the burden of student debt.

– Judith Scott-Clayton and Jing Li

Judith Scott-Clayton is Associate Professor of Economics and Education at Teachers College, Columbia University. Jing Li is Research Associate in the Department of Education Policy and Social Analysis at Teachers College, Columbia University.

This post originally appeared as part of Evidence Speaks, a weekly series of reports and notes by a standing panel of researchers under the editorship of Russ Whitehurst.

Notes:

[i] See Susan P. Choy and Xiaojie Li (2006), “Dealing With Debt: 1992–93 Bachelor’s Degree Recipients 10 Years Later,” Postsecondary Education Descriptive Analysis Report NCES 2006-156, Washington, DC: U.S. Department of Education; Erin Dillon (2007), “Hidden Details: A Closer Look at Student Loan Default Rates,” Washington, DC: Education Sector. Both studies utilized data from the Baccalaureate and Beyond 1992-93 graduate cohort, followed up after 10 years.

[ii] See Sara Goldrick-Rab, Robert Kelchen, and Jason Houle (2014), “The Color of Student Debt: Implications of Federal Loan Program Reforms for Black Students and Historically Black Colleges and Universities,” Wisconsin Hope Lab Discussion Paper, Madison, WI; Mark Huelsman (2015), “The Debt Divide: The Racial and Class Bias Behind the “New Normal” of Student Borrowing,” Washington, DC: Demos.

[iii] Marshall Steinbaum & Kavya Vaghul (2016), “How the student debt crisis affects African Americans and Latinos,” Washington, DC: Washington Center for Equitable Growth. The study used data on student loan delinquencies by zip code, from the credit reporting agency Experian, and matched this to information on racial demographics by zip code from the Census Bureau’s American Community Survey.

[iv] Fenaba R. Addo, Jason N. Houle, and Daniel Simon (2016), “Young, Black, and (Still) in the Red: Parental Wealth, Race, and Student Loan Debt,”Race and Social Problems, 8(1), 64–76; Michal Grinstein-Weiss, Dana C. Perantie, Samuel H. Taylor, Shenyang Guo, and Ramesh Raghavan (2016), “Racial disparities in education debt burden among low- and moderate-income households,” Children and Youth Services Review 65: 166–174.

[v] See Adam Looney and Constantine Yannelis (2015), “A Crisis in Student Loans?: How Changes in the Characteristics of Borrowers and in the Institutions They Attended Contributed to Rising Loan Defaults,” Brookings Papers on Economic Activity 2: 1-89; also see review of related evidence by Susan M. Dynarski (2016), “The trouble with student loans? Low earnings, not high debt,” Evidence Speaks Report, Washington, DC: Brookings Institution, https://www.brookings.edu/research/the-trouble-with-student-loans-low-earnings-not-high-debt/.

[vi] Danielle Douglas-Gabriel (2016),” Public-interest groups are calling on Education Dept. to track racial disparities in student lending,” Washington Post, https://www.washingtonpost.com/news/grade-point/wp/2016/09/15/public-interest-groups-calling-on-education-department-to-track-racial-disparities-in-student-lending/;http://www.studentloanborrowerassistance.org/wp-content/uploads/2013/05/ltr-sec-king-race-student-debt.pdf.

[vii] Meta Brown, Andrew Haughwout, Donghoon Lee, and Wilbert van der Klaauw (2013), “Do We Know What We Owe? A Comparison of Borrower- and Lender-Reported Consumer Debt,” Staff Report No. 523, New York: Federal Reserve Bank of New York.

[viii] Elizabeth J. Akers and Matthew M. Chingos (2014), “Are College Students Borrowing Blindly?” Washington, DC: Brown Center on Education Policy at Brookings.

[ix] Because loan amounts naturally grow over time with interest, estimates here are expressed in current dollars to avoid confusion. Hence, differences in undergraduate debt are current-dollar amounts as reported in 2007-08; differences in cumulative borrowing and amounts owed are as reported in 2012.

[x] Authors’ calculations using restricted Baccalaureate and Beyond 2007-08 survey data, 2012 follow up, measured in 2012 dollars. These average amounts include zeros for the 12 percent of black graduates and 29 percent of white graduates who never borrowed. The variable used, B2TOTDUE3, is not currently available via the publicly-accessible Quick Stats tool. The closest variable available in Quick Stats is B2BORAT (total amount borrowed), which understates the total gap due to differences in repayment rates.

[xi] See history of changes to student loan regulations by FinAid.org,http://www.finaid.org/questions/bankruptcyexception.phtml.

[xii] We decompose the gap with simple algebra, comparing differences in each component of total debt: undergraduate borrowing, graduate borrowing, and net repayments (the difference between total borrowed and total owed after four years).

[xiii] Valerie Wilson (2016), “African Americans are paid less than whites at every education level,” Washington, DC: Economic Policy Institute.

[xiv] We exclude enrollment in additional baccalaureate or sub-baccalaureate programs (the specific variable we utilize is B2HIENR, including categories 4 through 9).

[xv] We confirm that this broad trend is also noticeable in the ACS data, which covers a much broader set of cohorts and can be tracked annually. In the year 2000, only about 25 percent of all black BA graduates had any graduate enrollment compared to about 30 percent of white graduates. But by 2014 the rates had equalized, around 33 percent. The different percentages between the ACS and B&B are because the ACS includes BA graduates of all ages, not just those from a specific graduation cohort. Many of these individuals graduated from college long ago; thus, changes in enrollment that occur among recent cohorts will be muted when combined with older cohorts.

[xvi] Authors’ calculations using NCES Quick Stats with NPSAS:12 graduate student data, restricted to US citizens. For comparison, NPSAS:12 undergraduate data (again restricting to U.S. citizens) shows that 21 percent of black undergraduates and 11 percent of white undergraduates are in for-profit institutions.

[xvii] See Mark Kantrowitz, “History of Financial Aid,”http://www.finaid.org/educators/history.phtml.

[xviii] Jason Delisle (2015), “Don’t Just Blame For-Profit Colleges for Exploding Grad School Debt,” Forbes,http://www.forbes.com/sites/jasondelisle/2015/08/03/grad-school-debt/#56d1c5536fe0; Cumulative graduate loan debt for currently enrolled graduate students is $23,000 for enrollees at public institutions, $33,000 for those at for-profit institutions, and $36,000 for those at private not-for-profits. Authors’ calculations using NCES Quick Stats with NPSAS:2012 graduate student sample (restricted to U.S. citizens).

[xix] A comparison of NPSAS:2012 and NPSAS:2004 graduate enrollment estimates (produced via NCES Quick Stats) shows that graduate enrollments nearly quadrupled in the for-profit sector (from 105,000 to 388,000) while increasing by only 18 percent in the public and private non-profit sectors combined (from 2.3 million to 2.7 million).

[xx] Sudeep Reddy (2010), “Recession Exacerbates Race Gap,” Wall Street Journal,http://www.wsj.com/articles/SB10001424052748704292004575230543067586002.

[xxi] David W. Johnston and Grace Lordan (2014), “When Work Disappears: Racial Prejudice and Recession Labour Market Penalties,” CEP Discussion Paper No. 1257, London: Centre for Economic Performance.

[xxii] Authors’ calculations using NCES Quick Stats, B&B:08/12 data restricted to U.S. citizens.

[xxiii] Sandy Baum (2014), “Higher Education Earnings Premium: Value, Variation, and Trends,” Washington, DC: Urban Institute.

[xxiv] We pool data from the 2000-2014 ACS surveys, restrict the sample to 25-45-year-old high school graduates, and then regress ln(earnings) on degree attainment indicators as well as their interactions with race, gender, race, potential experience and experience squared. We find that the earnings premium for a graduate degree for whites, above and beyond a BA/BS, is 25 percent, while for blacks the premium is 33 percent. However, blacks also face a general wage penalty of 13 percent relative to whites.

[xxv] Paul Fain (2016), “Getting Tough with a Gatekeeper,” Inside Higher Ed,https://www.insidehighered.com/news/2016/06/16/education-department-recommends-eliminating-national-accreditor-many-profit-colleges.

[xxvi] Authors’ calculations using restricted B&B: 08/12 data. After limiting the sample to U.S. citizens who are employed full-time and not currently enrolled in 2012, we regress debt-to-income ratios on race indicators, an indicator for graduate attainment, interactions between race and graduate attainment, and include controls for age, gender, SAT/ACT scores if available, high school GPA, parental education indicators, undergraduate EFC, and undergraduate GPA. The 27 percentage point difference cited represents the sum of the coefficient on “Race:Black” (12 percentage points) and the coefficient on “GraduateDegree*Race:Black” (15 percentage points).

[xxvii] Authors’ calculations using NCES Quick Stats, B&B:08/12 data restricted to U.S. citizens.

[xxviii] http://www.studentloanborrowerassistance.org/wp-content/uploads/2013/05/ltr-sec-king-race-student-debt.pdf.

[xxix] Huelsman (2015).

[xxx] Authors’ calculations using NCES Quick Stats, Beginning Postsecondary Students:2003/09 data.

[xxxi] Addo, Houle, and Simon (2016).

[xxxii] This point has been made by Goldrick-Rab, Kelchen, & Houle (2014), as well as by Susan Dynarski (2014), “An Economist’s Perspective on Student Loans in the United States,” Economic Studies Working Paper Series, Washington, DC: Brookings Institution.

[xxxiii] Brandon A. Jackson and John R. Reynolds (2013), “The Price of Opportunity: Race, Student Loan Debt, and College Achievement,”Sociological Inquiry 83(3): 335-368.

[xxxiv] Susan Dynarski (2014), “An Economist’s Perspective on Student Loans in the United States,” ES Working Paper Series, Washington, DC: Brookings Institution.