Senator Elizabeth Warren (D-MA) announced an ambitious plan earlier this week that would cancel most outstanding student debt held by households making up to $250,000. Our analysis of federal data shows that this plan is likely to disproportionately benefit middle- and upper-middle-income Americans, as well as black families, at an estimated total cost of about $955 billion.

Warren’s proposal would forgive $50,000 of student debt for everyone living in a household with up to $100,000 in annual income and progressively smaller amounts for households with incomes between $100,000 and $250,000. We use data from the Survey of Consumer Finances (SCF), a nationally representative survey of households last conducted by the Federal Reserve Board in 2016, to calculate how student debt cancellation under Warren’s plan would be distributed to different income and racial and ethnic groups in the US. We focus on federal education debt, which accounts for approximately 90 percent of all student debt.

Distribution of loan forgiveness by income

We estimate that 66 percent of federal student loan dollars would be forgiven under Warren’s plan. Applying this estimate to the most recent total debt in the federal student loan portfolio ($1.447 trillion) yields a cost estimate of $955 billion dollars. This estimate is higher than the one in the economic analysis (PDF) provided by Warren’s campaign, which used a different methodology.

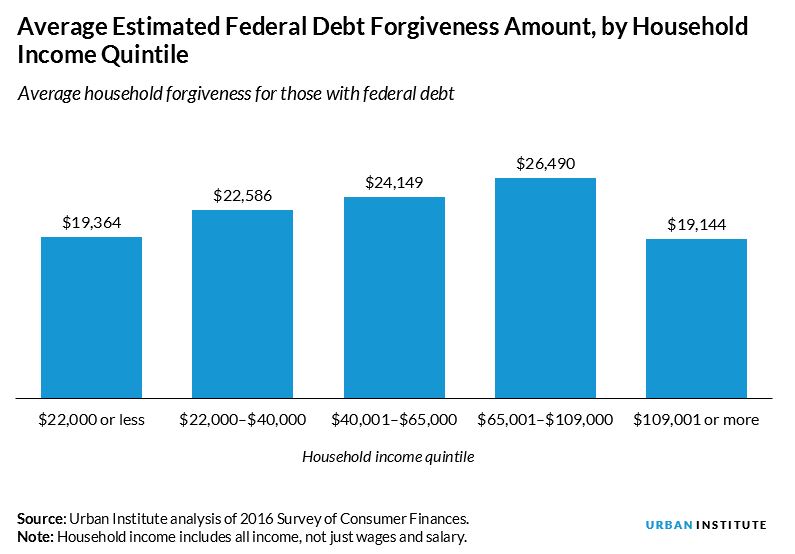

We first assess how Warren’s proposal would distribute the $955 billion in cancelled loans by calculating the size of the benefit for different income groups. We find that, for households with federal student debt, the amount of federal debt forgiven increases as household income increases but drops for households in the top income quintile, which receive the same average benefit as those in the lowest quintile. This finding reflects the fact that average borrowing increases with household income, but the Warren proposal reduces the benefit for families in the top income group (with no forgiveness for families earning more than $250,000, who make up about 5 percent of households).

If we look at total dollars rather than average forgiveness, the benefits skew even more toward the higher income groups because those households are more likely to have education debt in the first place (in addition to having larger amounts of debt). Just 16 percent of households in the lowest income quintile have any federal student loan debt, while 24 and 20 percent of households in the second-highest and highest quintiles have debt, respectively. Among households that have debt, the average bottom quintile household has about $25,600, while the average debt is $43,400 in the highest quintile.

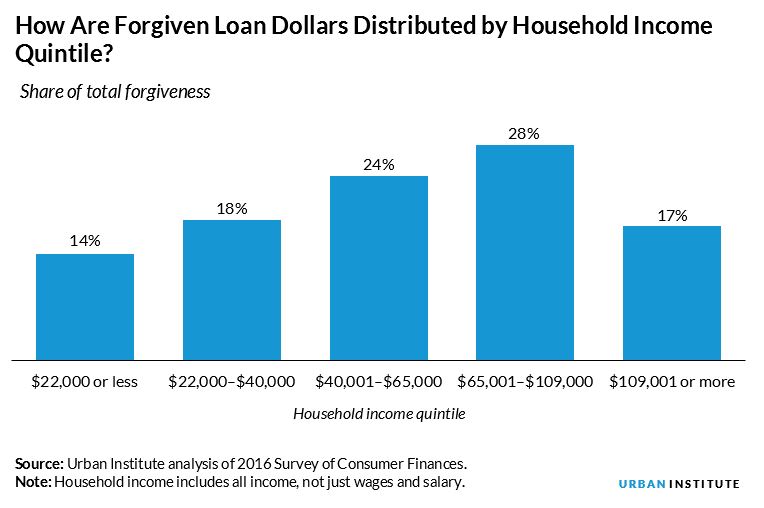

These patterns in borrowing by income result in 45 percent of cancelled loan dollars going to households earning less than $250,000 in the top two income quintiles and just 14 percent going to the bottom quintile. In other words, phasing out the benefit for higher-income households reduces the benefit for the top income group but does not tilt the benefits to substantially favor low-income households.

Distribution of loan forgiveness by race and ethnicity

Long-standing racial wealth gaps are closely connected to education debt. Warren’s proposal specifically cites the racialized nature of the debt issue and seeks to narrow racial wealth gaps, pointing out that “across all colleges, black students were on average nearly 20 percentage points more likely to need federal student loans.”

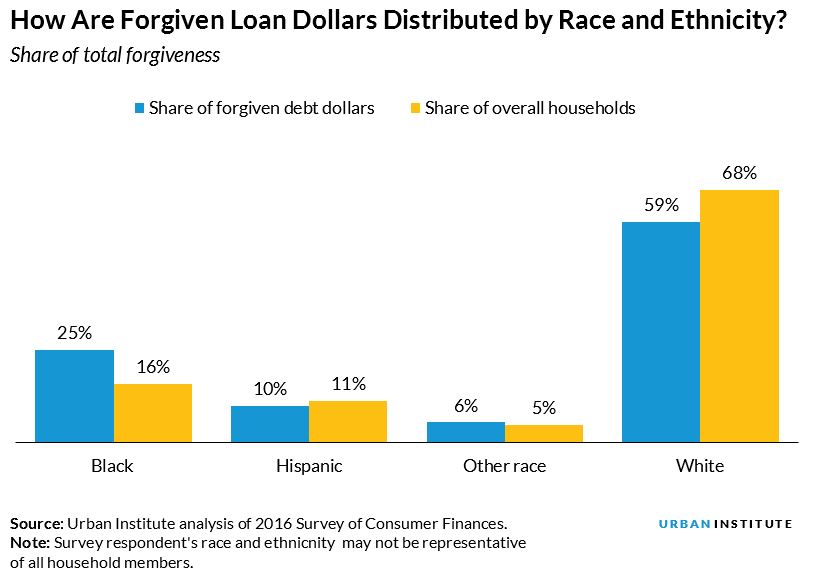

Our analysis finds that the proposal would disproportionately benefit black families: 25 percent of cancelled debt dollars would go to black households (16 percent of all households) and 59 percent would go to white households (68 percent of all households). Hispanic and other racial and ethnic groups (which are combined in the SCF to protect respondent confidentiality) are both projected to receive benefits that are roughly commensurate with their share of the population.

Loan forgiveness is just one portion of Senator Warren’s plan, which also seeks to eliminate tuition at public colleges, increase Pell grants, provide additional funding to historically black colleges and universities, and end federal aid to for-profit colleges. And other candidates are likely to release their own plans in the coming months. We will continue to evaluate how proposed reforms to federal higher education policy are likely to affect different groups of Americans and at what cost.

Additional statistics from our analysis, including results by education and age, are available to download here.

Matthew M. Chingos is a Senior Fellow at the Urban Institute. Kristin Blagg is a research associate in the Income and Benefits Policy Center at the Urban Institute, focusing on education policy.

This post originally appeared on Urban Wire.