Executive Summary

Congressional leadership and the Trump administration have put forward a plan (Framework) to “significantly” increase the amount of the Child Tax Credit, which is currently worth up to $1,000 per child to qualifying families. The credit presently phases out for higher income families and is partially refundable for some low-income families.

I place the Child Tax Credit in the context of the entire catalog of federal programs that result in spending on children and their families, including both tax expenditures and social programs. I describe how much is spent on children through each program; how much is for children under five years of age; how the expenditures are distributed across different family income levels; and current proposals by the Trump administration and Congress to modify these expenditures.

I find that, leaving aside health care as well as public and post-secondary education, the federal government spends approximately $217 billion annually through tax expenditures that are conditional on children and on social programs intended to support children. Of this total, roughly $73 billion goes to children under five.

With the exception of the Earned Income Tax Credit, present tax expenditures provide minuscule benefits to the poorest families. Benefits are concentrated in the middle to high ends of the income distribution. The Framework has the greatest potential to increase benefits for children and their families through changes in the Child Tax Credit, but the plan is vague on critical details. Raising the dollar value of the Child Tax Credit is important, as is promised in the Framework, but so is extending its benefits fully to low-income families.

I make four recommendations for legislative actions that would improve prospects for families with young children: 1) Spend more on families with children, particularly young children. 2) Make such expenditures more progressive so that families with the greatest needs receive more assistance. 3) Simplify what is now an incoherent and confusing patchwork of social programs and tax expenditures. 4) Transform spending on social programs for children from lower-income families so that more money goes directly to individuals and less to social service agencies.

Background on the child tax credit

There is bipartisan support, accumulating since at least the Roosevelt administration, for a significant federal role in supporting the welfare of children and families. Young children and their families are a particular priority for additional spending and reforms. This is based on a widely shared understanding of the importance of the early years. This understanding is derived from research, consideration of the unique needs for childcare of working parents with young children, and acknowledgement of weaknesses in our present patchwork of spending and services.

The next federal effort to increase support for children and their families will likely take the form of an expansion of the Child Tax Credit, [1] which is currently worth $1,000 per child at tax filing time for qualifying families that would otherwise have at least that much due in taxes (details below). It was first passed into law in the Clinton administration with 90 percent of the House and 92 percent of the Senate voting in support. [2] Subsequent legislation in the George W. Bush and Obama administrations increased the generosity of the credit and made it permanent. [3] As I document subsequently, its benefits flow disproportionately to families in the middle of the income distribution.

Expanding the Child Tax Credit is firmly on the list of items that Congressional leadership aspires to include in tax legislation. This is because it, first, aligns with the understanding I described above; second, would result in a meaningful tax benefit for middle-income families and thereby soften criticism that the benefits of the proposed tax package flow disproportionally to the rich; and third, has the backing of the Trump administration. [4]

The legislative outcome of present efforts to further increase the Child Tax Credit will play out in a political arena in which the prospect of winning or losing typically comes to take precedence over (and sometimes eclipses entirely) the substantive goals that originally motivated legislative interest. Political reality is, of course, a critical ingredient in making government policy. But to the extent possible, legislation needs to be framed by knowledge of what government is already doing, serious and informed policy formation, and evidence that bears on likely consequences.

A catalog of tax and program spending on children and their families

In an effort to balance political calculations with continued focus on substantive policies to increase support for young children and their families, I place the Child Tax Credit in the context of the entire catalog of federal programs that result in spending on children and families. I describe how much is spent on each of those programs (and specifically how much is spent on children under five years of age), how the expenditures are distributed across different family income levels, and current proposals by the Trump administration and Congress to modify these expenditures. I end with a list of possibilities for legislative action that could strengthen the positive impacts of federal programs on young children and their families without, necessarily, increasing their costs.

The largest federal expenditures on children and families, ignoring Medicaid, CHIP and the education system, are through provisions of the tax code that are tied to a taxpayer’s income, number of dependents, and the amount parents spent on the care of their children. The largest of these expenditures include a dependent exemption per each child of $4,050 of a family’s income; the child tax credit of up to $1,000 per child; pre-tax flexible spending accounts for child care; deductions for payments made to child care providers; and, for families of the working poor, so-called refundable credits through the Earned Income Tax Credit and the Additional Child Tax Credit (the family can get more money in their tax refund than they paid in taxes).

Child care expenses and the needs of low-income families with children are also addressed by a number of direct federal programs that are funded through line item discretionary or mandatory budgets. The largest of these are Head Start, the Child Care and Development Fund, Temporary Assistance for Needy Families, the Child and Adult Care Food Program, the Supplemental Nutrition Assistance Program, and various housing assistance programs.

There are also significant federal expenditures for the health care of young children through Medicaid and the Children’s Health Insurance Program, and for public and post-secondary education. My interest, in keeping with current deliberations in Congress, is on elements of the tax code that provide direct financial support to families based on their having children and on social programs that support children. I exclude federal health care and education expenditures from further consideration. [5]

Table 1 lists each federal program within the focus I’ve described that has an annual level of expenditure conditional on children that is greater than $1 billion. There are dozens of smaller programs I ignore for the sake of economy of presentation. [6] The columns in the table address: a) the vehicle by which funding is delivered (e.g., tax expenditure vs. social program); b) the particulars of that funding vehicle (e.g., payments to individuals vs. program providers or states); c) the dollar value of the benefit to a family; d) whether the tax benefits are refundable (provide refunds to low income families in excess of their tax liability); e) whether the benefits are progressive (inverse to family income); f) the total annual program expenditure that is conditional on children (e.g., spending on housing vouchers that goes to families without children is excluded); and g) the estimated portion of the total expenditure that goes to children under five years of age. Additional information on the table and its values is found in the Appendix.

The total of the expenditures for children of all ages (the next to last column in Table 1) is $217 billion, whereas the total for children under five years of age (the last column) is $73 billion. There are approximately 20 million children in the U.S. under five years of age. [7] Thus, the federal government spends approximately $3,650 per child per year on children under age five or on families based on their having children under five. Of course, money that flows to families through the dependent exemption, the child tax credit, and the earned income tax credit need not be spent on children even when the amount a family receives is conditional on their having children. There is a substantial body of research indicating that such cash transfers benefit children in low-income families. [8] Whether financial supports to parents from the federal government that are constrained to be used only on children have larger impacts on children than cash transfers to the family that do not have to spent on children or whether both together function best is an open and important question.

Distributional characteristics of federal programs intended to support families with children

The Progressive column of Table 1 provides a gross description of whether each program is tilted to favor less wealthy families, i.e., is progressive. Whereas all of the non-tax code programs, other than Social Security, are designed specifically to serve the needs of low-income families, several of the tax code programs are either regressive, or only slightly progressive, or actually exclude the lowest income families.

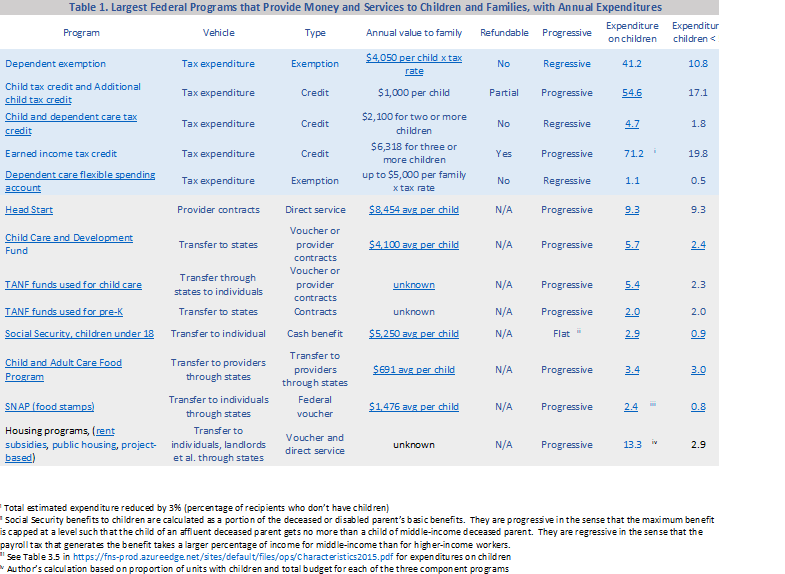

Figure 1 displays the distribution of benefits from the dependent exemption by quintile of family income. [9] The break points between each quintile in 2017 dollars are, in thousands: $24.9; $48.3; $85.6; & $149.6 (e.g., the income dividing line between families in the first and second quintile is $24,900).

Only 1.5 percent of the dependent exemption goes to families from the lowest income quintile whereas 58 percent of the benefits flow to families in the top two quintiles of income. In other words, most of the money from the dependent exemption goes to families that need it least, whereas hardly any of it goes to the poor. [10]

Likewise, the Child and Dependent Care Tax Credit, which I do not depict in a graph, is heavily tilted towards more affluent families: The top quintile of income receives 35 percent of the total expenditure whereas the lowest quintile receives 1 percent. [11]

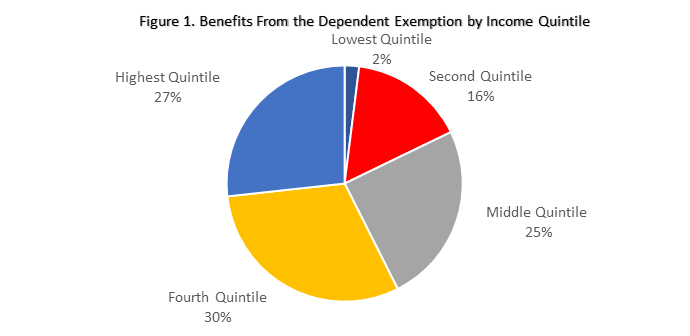

As illustrated in Figure 2, the Earned Income Tax Credit, in contrast to the Child and Dependent Care Credit and the Dependent Exemption, is progressive and focused on lower income families. [12] Virtually no benefits are received by families in the top two income quintiles.

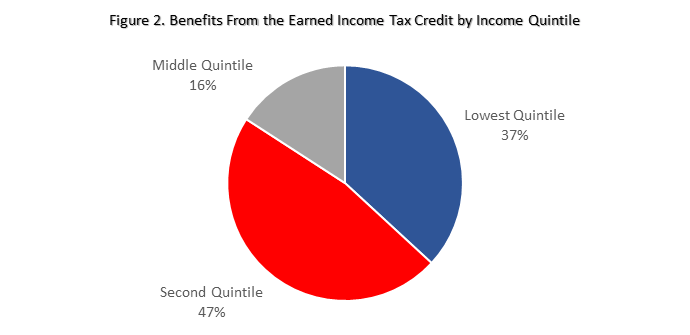

The Child Tax Credit is the curious tax expenditure in terms of distribution of benefits. It is also the very program that is currently a legislative target for expansion. As illustrated in Figure 3, the benefits are concentrated in the middle of the distribution of family income. The middle quintile gets the largest slice of the pie, 40 percent. The second and fourth quintiles split most of the remainder. The poor and the rich get only slivers. [13]

The paltry payout of the Child Tax Credit to low-income families occurs despite the benefit being partially refundable under a provision of the law called the Additional Child Tax Credit. For example, a family with two children with an income of $12,000 would claim a child tax credit of $1,000 for each child — $2,000 in all. If the family owes no taxes, as is the case for most low-income families, they would receive a refundable credit equal to 15 percent of every dollar they earn over $3,000. Thus, this particular family would receive a payment of $1,350 [($12,000 – $3,000) * .15], which they would receive in the same form as a regular tax refund. If they had sufficient income to owe taxes of $2,000 or more they would receive the full credit of $2,000.

The net result of the calculations under the Additional Child Tax Credit is that the very lowest income families receive nothing and those doing better but still living in poverty receive less than they would if they were making a modestly higher income. The refundability provisions of the Child Tax Credit were apparently designed with the priority of incentivizing work in low-income families. They do not provide the greatest benefit to the families with children who are in greatest financial need.

Current proposals for tax reforms

Raising children is expensive – about $10,000 year for one child for two-parent families earning less than about $60,000 a year. [14] Young children place a particular stress on family income: 60 percent require child care because their parent(s) work outside the home. [15] The costs of child care are high – about $10,000 a year for full time center-based care. [16] There appears to be wide agreement that the federal government should do more to support the needs of families during the most formative and expensive years of child growth and development.

At this point in time, all the action on increases of support for families with children is in the area of tax expenditures. I focus here on coalescing efforts by the Trump White House and the Republican Congressional leadership on tax reform, which include provisions that would affect the Child Tax Credit. [17] Several specifics of the proposals that are in play are vague. And prospects for providing additional tax relief to parents are up against the political appetite to make large tax cuts elsewhere while maintaining some constraints on deficits.

That said, the Child Tax Credit may be raised by at least $500 (from $1,000 to $1,500 per child). The Big Six Unified Framework (named for the four Congressional leaders and two administration officials who are its architects) “significantly increases” the Child Tax Credit without specifying a dollar figure. The “significant increase” is paired in the Framework with almost doubling the standard deduction (from $12,700 to $24,000 for a married couple filing jointly), which would also benefit young children by reducing their family’s taxes. However, what is gained by families from an expanded Child Tax Credit and an increased standard deduction is largely taken back by the elimination of the dependent exemption. As Elaine Maag at the Urban-Brookings Tax Policy Center puts it, the proposed increase in the Child Tax Credit under the Framework would “provide no additional benefit for very low-income families; roughly replace the Framework’s proposal to repeal personal exemptions for most middle-income families; and slightly increase taxes for higher income families.” There is, she says, “Nothing to see here.” [18] However, there is hope for better deal for lower-income families in the vague promise in the Framework of “additional tax relief that will be included during the committee process.”

Possibilities for doing more and doing it better

Spend more. A tax reform proposal that provides “nothing to see” for families with children is not useful if the goal is to provide more support for children and their families. There are many competing values and goals for tax reform. It may be useful to for those in the lead to keep in mind that the empirical basis for positive returns to individuals, children, and the economy from putting more money in the hands of lower-income families is relatively strong [19]. In comparison, evidence on the impact of other items on the table such a repatriation of offshore earnings is weak or contrary. [20]

Because reducing taxes on families is an easy sell to voters whereas reducing taxes on large businesses is not, we may be in a situation where evidence on what works economically and political expediency are aligned. If the Child Tax Credit is to be the only vehicle in tax reform intended to provide direct benefits to lower- and middle-income families with children, it should be increased by at least $1,000 – becoming a maximum $2,000 per child. This would appeal to lower- and middle-income voters and would have a positive impact on the economy.

Help most those in greatest need. Per the descriptions of progressivity in Table 1, the federal government’s tax expenditures on children and their families disproportionately serve middle- and higher-income families (with the exception of the Earned Income Tax Credit). To be specific, only about 2 percent of the benefits from the Child Tax Credit, Dependent Exemption, and Child Care Credit flow to families in the lowest quintile of income. Even with the Earned Income Tax Credit, designed to help low-income families, those in the lowest quintile of income receive a smaller percentage of the distribution than those in the second lowest quintile.

As indicated previously, proposed increases in the Child Tax Credit under the Framework have little net impact on families in the lowest quintile of income – the language of the Framework is that “the credit will be refundable as under current law.” To the extent that we are going to use the tax code as a vehicle for supporting children and their families, we should spend money where it will do the most good and where, absent federal spending, bad things will happen. In other words, spend the most on the poor.

In practical terms, this suggests eliminating tax expenditures that are not substantially progressive and that do not load most benefits into the left side of the income distribution. The Dependent Exemption, Child and Dependent Care Credit, and Flexible Spending Account would be eliminated under this design principle. The Child Tax Credit could remain, but would need to become fully refundable and applicable to payroll taxes (Social Security and Medicare) to allow families in the lowest quintile of income to receive at least their prorated share of benefits. It might also be increased more for younger than for older children because parents have greater expenses for young children. [21]

Simplify. It took me the better part of a week to pull together the information in Table 1, and this is a topic I know something about. Heaven help the individual with many other responsibilities who has to wade through this thicket as a consumer of services, policymaker, or manager. The nation’s interests are not well served by the federal government having five major tax expenditures and seven major social programs (and another couple of dozen smaller programs) intended to support the needs of children and their families. This is a recipe for what we have, a confusing smatter of programs and spending streams that don’t form a coherent system that can be managed, evaluated, and improved over time.

My recommendation on the tax expenditure side is to combine the Child Tax Credit and the Earned Income Tax Credit into a single program, and eliminate all the other tax expenditures listed in Table 1. The combined tax credit programs would beef up benefits at the lower end of the scale by spending more and providing for fully refundability. It would retain benefits for middle income families but, as is the case presently, fade out those benefits so that families in the top two quintiles receive very little.

Support families directly. The tax expenditures in Table 1 have, from my perspective, the consistent advantage compared to the social program expenditures in Table 1 of putting money directly into the pockets and bank accounts of families with children. There are no institutions and bureaucracies that sit in between families and these benefits other than those necessary to collect and distribute the funds – in this case the IRS.

In contrast, most of the social programs listed in Table 1, e.g., Head Start, involve intermediaries between the federal benefits and their intended beneficiaries. Families get a service paid for by the taxpayer but they have to deal with a welfare agency or service provider under government contract to access it.

One way forward for simplification and increases in the productivity of the federal investment is to make social programs intended to support lower income families with children more like tax expenditures – putting more money directly in the hands of parents to spend on the care and development of their children and less money directly in the financial accounts of states, welfare agencies, and social service providers. As former Senator Daniel Patrick Moynihan used to say, having government bureaucracies dispense social services to the poor is like “feeding the sparrows by feeding the horses.” [22]

Conclusions

Present plans for federal tax cuts and reforms are predicated, in part, on helping families by directly putting more money in their pockets. Those plans need to be fleshed out in ways that provide greater benefits for children in families most in need if tax reform is to have maximum impact on economic growth and the opportunities the nation offers to families that are struggling economically. The coming legislative debate and public conversation on the details of tax reform provide a significant opportunity to provide more straightforward and effective supports for the needs of children and their families. Tax reform is an end in itself, but it can also be the foundation for future comprehensive reform of the entire federal investment in children.

Appendix

Table 1 includes a list of programs with an annual expenditure of at least $1 billion that goes to children or to families conditional of their having children. For example, the standard deduction, for provides a tax benefit to many families with children but it is not conditional on the family having children, as so it is not included in Table 1. A hyperlink associated with each program listed in the Program column in Table 1 provides basic details on the nature and requirements of the program. Budget information for each program is available through hyperlinks associated with the expenditure totals listed in the last two columns of the table.

The second column in the table, entitled Vehicle, provides information on the funding mechanism by which each program operates. In that context, a tax expenditure refers to spending through the tax code tied to individual tax returns. The other vehicles involve either direct funding of service providers by the federal government, e.g., Head Start, or transfers to states from the federal government, and through them to providers or individuals, e.g., the Child Care and Development Fund. Tax expenditures vs. social programs are grouped separately in the table and color-coded.

The Type column provides additional detail on the funding mechanism. Definitions for the type of tax vehicle described in the table will be useful for readers not familiar with the arcane language of the tax code: Exemption refers to specified income that is not subject to federal tax. The value of an exemption is a function of the taxpayer’s marginal tax rate such that $1,000 in exempt income is worth $350 to someone in the 35 percent tax bracket (who avoids payment of $350 in tax due), but only $150 to someone in the 15 percent bracket. Deductions function in the same way as exemptions in that their value goes up with the taxpayer’s marginal tax rate. But, unlike exemptions, they arise from documented expenses. For example, a taxpayer must have child care expenses (and itemize them on his or her tax return) to receive a deduction whereas the same taxpayer does not have to incur any particular expense or itemize to take advantage of the dependent exemption. Credits are the tax expenditure of most value to the taxpayer in that they are direct reductions of taxes owed. Thus, a $1,000 tax credit is worth $1,000 to any taxpayer who has at least that much tax due. Credits can also be refundable (exceed the value of the tax due and result in an additional “refund” to the taxpayer), about which more information will follow.

Type entries for the non-tax programs in Table 1 are self-explanatory, with the exception, perhaps, of voucher. Voucher refers to a program that allows the recipient to choose and pay a provider, in whole or in part, using some form of chit for government funds. For example, states typically spend most of their federal Child Care Development Fund budget by assigning a voucher of a particular dollar value to a parent receiving welfare, who can then use it to purchase child care from a variety of sources. Head Start, in contrast, involves contracts with agencies to provide Head Start programs. The parent is not a party to the financial transaction. Likewise, the SNAP program (food stamps) provides nutritional support to families with young children through vouchers whereas the Child and Adult Care Food Program, which has related goals of underwriting the costs of food for children from lower-income homes, is carried out through transactions between child care centers and government.

Annual value to family provides either a statutory amount of federal benefit (in the case of tax expenditures) or the average expenditure per child (for programs in which total expenditure and number of participants are known but benefits vary with characteristics of individual recipients). When the statutory tax benefit varies with family size, the tabled value is the maximum. Statutory amounts are taken from the 2016 tax year whereas average values are from various agency reports.

Refundable indicates whether the taxpayer can receive an additional cash transfer based on family income and size after his or her tax obligation reaches zero. This is a form of negative income tax such that the annual tax return provides an opportunity for poorer families to receive an income boost from the federal government in addition to any refund they are due on taxes they have paid.

Progressive and Regressive as used in Table 1 and the text characterize each program in terms of whether its generosity depends on family income, whereas in formal tax parlance progressive and regressive refer to whether tax rates change with income and in which direction. In my usage a “progressive” program provides larger dollar amounts to less affluent families, whereas a “regressive” program does the opposite. For example, the dependent exemption is regressive benefit because the dollar value depends on the taxpayer’s tax bracket – a family in the 35 percent bracket avoids about $1,400 of tax for each dependent whereas a family in the 15 percent bracket avoids only about $600. The earned income tax credit, in contrast, is progressive – it fades out based on earned income and number of children, and is eliminated entirely once income reaches about $48,000 for a married couple with three or more children.

The next to the last column in Table 1 presents the total annual federal expenditure for the program that is a direct benefit for children or is conditional on children. For programs that provide a benefit based on family size rather than children in particular, e.g., food stamps and housing assistance, the total expenditure in Table 1 is that attributed to children in federal administrative reports or public data.

The last column in the table is an audited or estimated portion of the total expenditure for children that is for children under age five. In some cases, the expenditure for children under five is the entire expenditure, e.g., Head Start. In other cases, it is an estimate based on federal agency survey or administrative data. In the remaining cases, it is derived by taking the fraction of the total expenditure that the first four years represent of the total years of a child’s eligibility. For example, the Child Care Credit applies to children under 17 years of age. Thus, the expenditure on children under five is estimated as 5/16 of the total expenditure.All the dollar figures in Table 1 are taken from the most recent year for which I could find public data. Differences between 2015 and 2016 data, for example, are unimportant for the points made in this paper, but might well be important for other purposes.

— Russ Whitehurst

Russ Whitehurst is a Senior Fellow in the Center on Children and Families in the Economic Studies program at the Brookings Institution.

Russ Whitehurst is a Senior Fellow in the Center on Children and Families in the Economic Studies program at the Brookings Institution.

This post originally appeared as part of Evidence Speaks, a weekly series of reports and notes by a standing panel of researchers under the editorship of Russ Whitehurst.

The author(s) were not paid by any entity outside of Brookings to write this particular article and did not receive financial support from or serve in a leadership position with any entity whose political or financial interests could be affected by this article.

Notes:

1. https://www.treasury.gov/press-center/press-releases/Documents/Tax-Framework.pdf

2. http://projects.washingtonpost.com/congress/105/house/1/votes/350/

3. https://fas.org/sgp/crs/misc/R41873.pdf

4. http://www.politico.com/story/2017/10/09/ivanka-trump-takes-on-taxes-243604

5. Any federal funds that make their way to individuals or social programs can affect children and families. I restrict my attention to social programs that have an explicit focus on children and tax expenditures that are conditioned on a count of children in a family or family expenditures made by families on their children’s care.

6. https://www.gao.gov/products/GAO-17-463

7. https://www.childstats.gov/americaschildren/tables/pop1.asp

8. https://www.brookings.edu/wp-content/uploads/2017/03/es_20170309_whitehurst_evidence_speaks3.pdf

9. Family income as I use the term here is cash income plus tax-exempt employee and employer contributions to health insurance and other fringe benefits, employer contributions to tax-preferred retirement accounts, income earned within retirement accounts, and food stamps.

10. http://www.taxpolicycenter.org/sites/default/files/alfresco/publication-pdfs/1001478-Who-Benefits-From-the-Dependent-Exemption-.PDF

11. http://www.taxpolicycenter.org/model-estimates/individual-income-tax-expenditures-april-2017/t17-0141-tax-benefit-child-and

12. http://www.taxpolicycenter.org/model-estimates/distribution-individual-income-tax-expenditures-2015-model-version-0515/tax-28

13. http://www.taxpolicycenter.org/model-estimates/options-reforming-child-tax-credit/distribution-benefits-child-tax-credit-under

14. https://www.cnpp.usda.gov/sites/default/files/crc2015_March2017.pdf

15. https://www.brookings.edu/research/why-the-federal-government-should-subsidize-childcare-and-how-to-pay-for-it/

17. https://www.treasury.gov/press-center/press-releases/Documents/Tax-Framework.pdf

18. http://www.taxpolicycenter.org/taxvox/child-tax-credit-unified-framework-nothing-see-here

19. https://www.brookings.edu/wp-content/uploads/2016/07/Family-support3.pdf

20. https://fas.org/sgp/crs/misc/R40178.pdf

21. https://www.urban.org/research/publication/analysis-young-child-tax-credit

22. http://www.washingtonpost.com/wp-dyn/content/article/2010/10/01/AR2010100105262.html