First starting in West Virginia, a wave of teacher strikes has now spread to Arizona, Kentucky, Oklahoma, and North Carolina. The proximate cause would seem to be teacher salaries, which in recent years have stagnated in many states. A careful look at the situation in Arizona, however, sheds light on why teacher pay isn’t meeting expectations.

Teacher salaries in Arizona have not just stagnated but actually declined, but there are other forms of compensation such as pension and health benefits that are often left out of the conversation. Retirement costs in particular have been rising, and these increased costs have disproportionately gone to paying down pension debt instead of pre-funding the pension benefits that today’s teachers are accruing. This same pattern is evident throughout most of the nation: Although pension costs are rising, teachers’ retirement benefits have been steady or fallen.

How is it that teacher pay has stagnated while pension costs have gone up?

Most public workers, including teachers, belong to defined benefit plans. Under these plans, one’s pension benefit is a function of his or her salary and years worked. Teachers in Arizona enroll in the Arizona State Retirement System and will receive a pension that, at least in theory, should be fully pre-funded by teacher and employer contributions. Every year, actuaries estimate the required contributions to pre-fund newly earned benefits (so-called “normal costs”) and amortize any unfunded liabilities for benefits earned in the past. In general, the employee and employer each pays half the total required contribution rate.

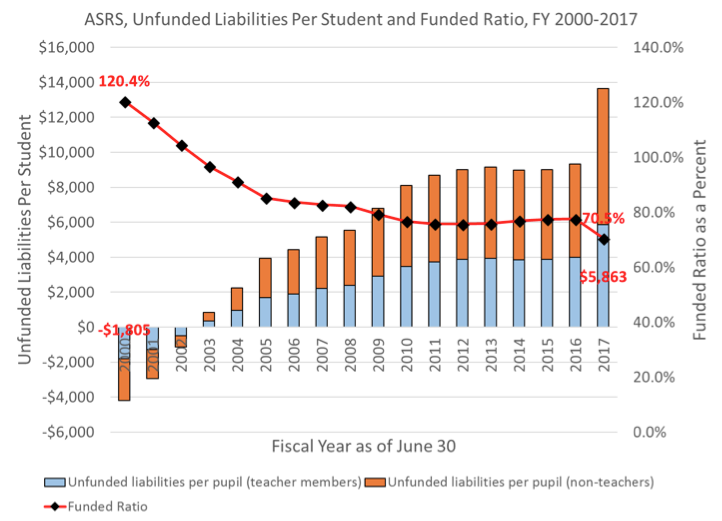

In 2000, the Arizona State Retirement System (ASRS) ran a surplus of $3.6 billion, and its funded ratio was 120 percent. That is, for every dollar the system owed for retirement benefits, it had $1.20 on hand to cover these obligations. Moreover, contribution rates were very low. Teachers and employers each contributed just 1.92 percent of payroll to the pension fund.

That’s a dramatically different picture from most public employee pension funds today—including Arizona’s. The system has accrued substantial unfunded liabilities, and contribution rates have increased rapidly. ASRS now runs a deficit with more than $15.4 billion in unfunded liabilities, or almost $6,300 for every household in the state.

The system covers public employees in general, and K-12 employees comprise about 43 percent of the system’s membership. Thus, the teacher’s share of unfunded liabilities is about $6.6 billion, or roughly $5,800 per student. To put this amount in perspective, this represents more than half of the state’s $10 billion K-12 budget.

Sources: Arizona State Retirement System actuarial valuations, various years; National Center for Education Statistics, U.S. Department of Education; author’s calculations

Note: Sharp decrease in funded ratio and increase in unfunded liabilities from FY 2016 to FY 2017 was partly due to the system lowering its assumption about the rate of return on investments from 8 percent to 7.5 percent

The system’s funded ratio (a metric commonly used to gauge a system’s sustainability) declined from 120 percent to 70 percent, a remarkable swing over less than two decades. How did it happen? One factor is that the system’s return on investments fell below the system’s target rate in many of those years.

Let’s take a closer look at the consequences of this shortfall in Arizona.

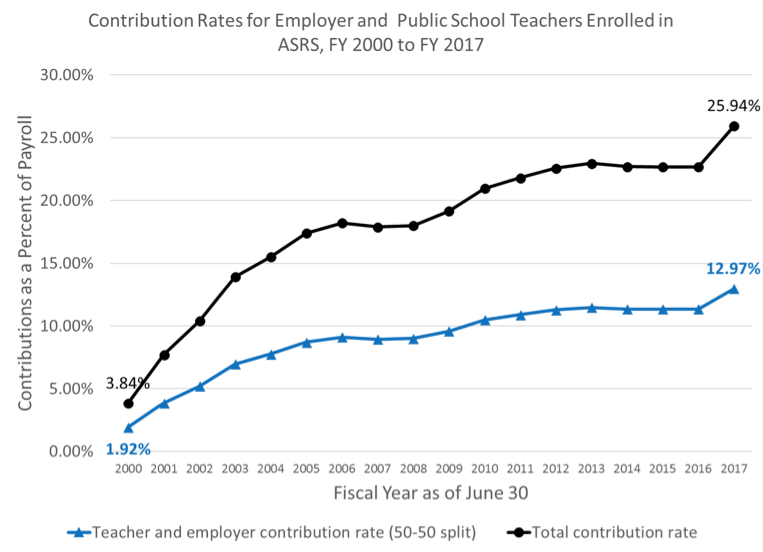

The total contribution rate for pension benefits for Arizona public school teachers in 2000 was 3.84 percent, and teachers and employers pay half, or 1.92 percent of pay. By FY 2017, the total required contribution rate increased almost seven-fold to 25.94 percent (the teacher share is 12.97 percent of pay).

Sources: Arizona State Retirement System actuarial valuations, various years

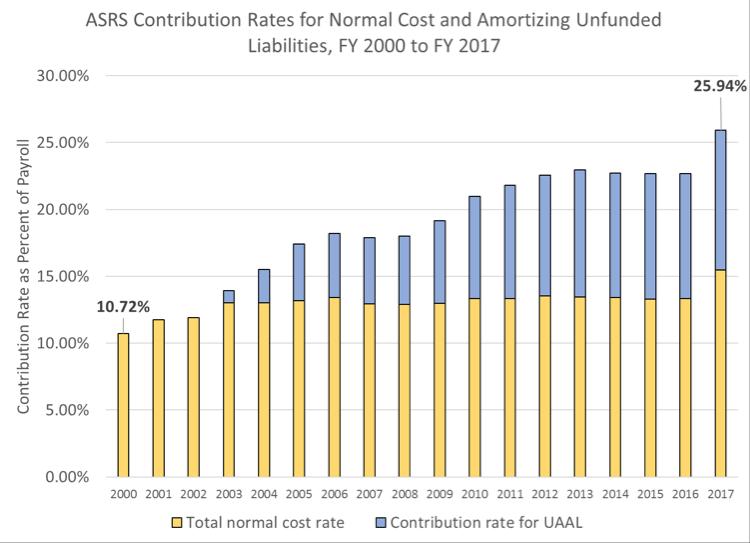

This increase, however, isn’t due to more generous retirement benefits. (If that were the case, we might not be having conversations about teacher strikes) Rather, a significant portion of contributions now go toward paying down unfunded liabilities.

Typically, in pension accounting all contributions made by a worker are used to fund normal costs (the cost of funding pension benefits accrued by teachers this year) while employer contributions comprise two components: remaining normal costs and amortizing unfunded liabilities (like paying a home mortgage or credit card debt).

In 2000, all contributions went toward normal costs only, as the system had no unfunded liabilities to amortize. This was also the case in 2001 and 2002, though the surpluses were smaller. By 2003, the system was no longer fully funded, and a small portion, just 13 percent of the required employer contributions, went toward amortizing this debt. Almost 90 percent of those contributions were paid to prefund pension benefits accrued by that year’s cohort of active teachers.

Sources: Arizona State Retirement System actuarial valuations, various years

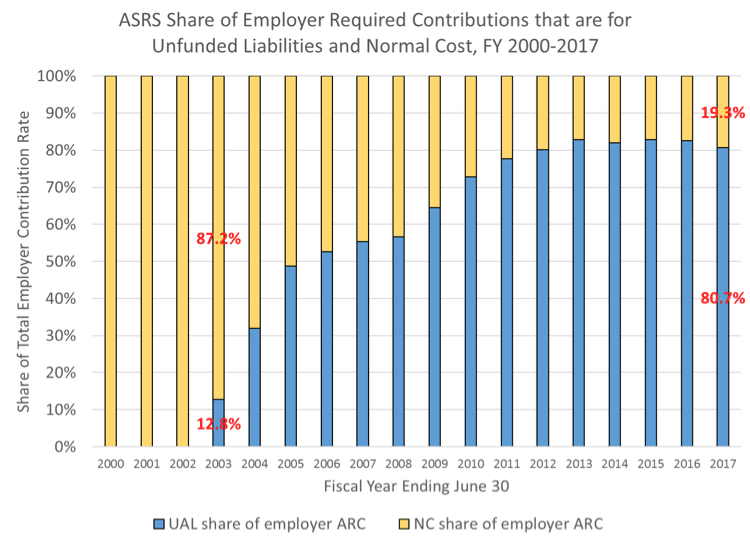

The share of contributions for unfunded liabilities rapidly increased, and today these shares have switched. For each dollar of contribution, 20 cents are paid for normal costs while 80 cents are used to pay for the system’s legacy costs.

Sources: Arizona State Retirement System actuarial valuations, various years; author’s calculations

This comes at a potentially large opportunity cost for teachers. In 2003, a teacher making $50,000 contributed $3,480 to the pension fund, and the employer contributed the same amount, for a total of $6,960. Every dollar contributed by teachers was used for normal costs. For each dollar of employer contributions, 87 cents were used to pre-fund pension benefits accrued by teachers that year while 13 cents of every dollar of employer contributions paid down the plan’s accrued unfunded liabilities. [1]

In FY 2017, a teacher making $50,000 and her employer each contributed $6,485, for a total of $12,970. This is almost twice the amount contributed by teachers and employers in 2003, even though normal costs increased by only 44 percent. Accrual of unfunded liabilities drove costs up. As in past years, every dollar of teacher contributions went to pre-funding benefits accrued by teachers that year. But now 80 cents of every dollar contributed by employers, or $5,325, was used to pay down unfunded liabilities. The teacher’s take home pay could have been 10 percent higher if not for the debt.

Just a small part of contributions made by teachers and their employers today are going toward paying for benefits that teachers today accrue with work. Most of those contributions are instead going toward paying down the system’s debt. Teachers and taxpayers today are paying for sins made in the past.

One solution to the funding issues embedded in DB plans is to offer a plan where contributions are tied directly to benefits, such as a defined contribution plan. With traditional defined benefit plans, they’re not. But this alone will not solve today’s debt problem—it would only help to stop the bleeding.

Even if states were to pass meaningful pension reform, they would still have substantial unfunded liabilities on the books. Workers and taxpayers today and in the future are on the hook. Although there’s no silver bullet, states would do well to consider policies that provide relief from budgetary pressures stemming from pensions and other fiscal challenges.

One option is educational choice. Although often criticized for draining money from public school systems, private school choice programs in fact have generated substantial taxpayer savings over the last several decades. A recent paper I wrote looked at 10 tax-credit scholarships in seven states and estimated they generated up to $3.4 billion in taxpayer savings through FY 2014. That represents up to $3,000 in savings for each scholarship. Another analysis looked at 10 voucher programs through FY 2011 and estimated those programs saved taxpayers $1.7 billion—about $3,400 on average for every voucher awarded. In other words, these programs can act as kind of release valve for states’ financial pressures.

Our teachers deserve better representation not only from their elected public officials, but also from those individuals negotiating on their collective behalf. Any discussion of teacher compensation needs to include the whole picture, including contributions made on their behalf for retirement benefits, and where those contributions are going. These systems need more transparency so teachers understand what they’re paying into, what they’ll get out of the system, and how long it will take.

Mere across-the-board raises, like the ones that followed the teacher strikes in Arizona and other states, fail to address the systemic problems with how teachers are compensated and how these systems are rigged against new and mobile teachers. There are numerous reasons for enacting pension reform, such as the inherent uneven distribution of benefits under many plans, cross-subsidization of benefits within and across cohorts, and intergenerational inequity that they create. Improving teacher compensation should be another compelling reason for any lawmaker to seek reform.

— Martin Lueken

Martin F. Lueken, Ph.D. is the Director of Fiscal Policy and Analysis at EdChoice.

Note:

1. In 2000-2002, the plan was overfunded, and the total contribution rates those years were less than the normal cost rates. Actuaries determined that the percent of pay needed to amortize unfunded liabilities was negative and, therefore, the total contribution rate was less than the normal cost rate of the plan.