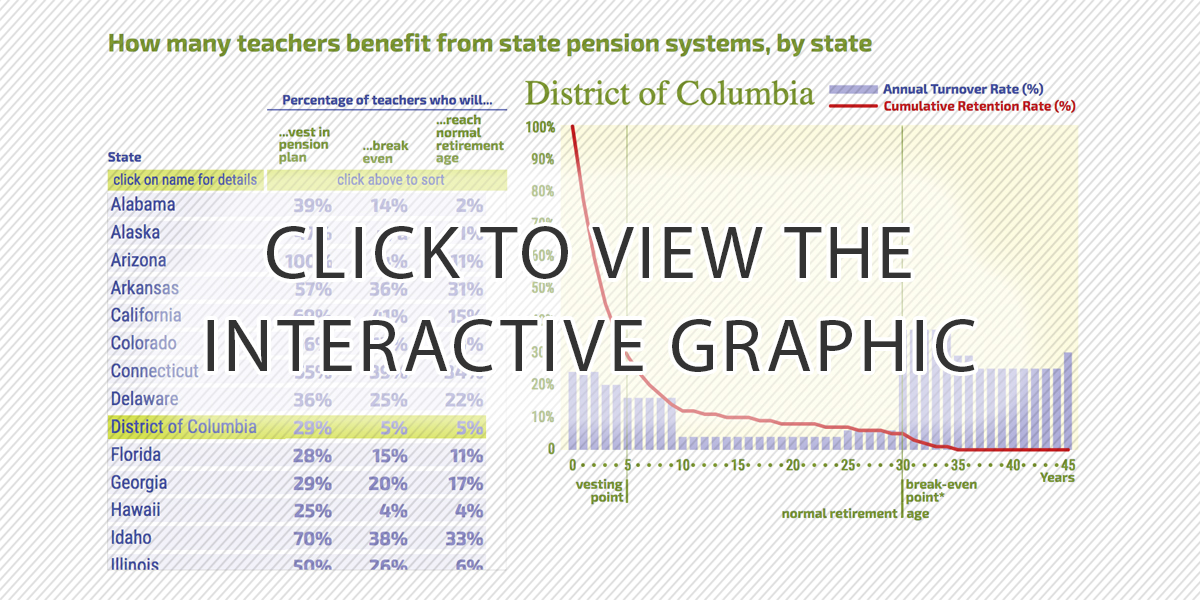

In our recent Education Next report, “Why Most Teachers Get a Bad Deal on Pensions,” my colleague Kelly Robson and I analyzed state pension plan turnover assumptions to look at two key milestones, the point when teachers first qualify for a pension, and when they become eligible for normal retirement. On the front end, we found that states assume less than half of all new teachers will teach long enough to qualify for a pension (that is, they won’t reach the “vesting” point). Moreover, no state assumes that teachers on the cusp of vesting will change their behavior in order to qualify for a pension.

On the back end of a teacher’s career, other researchers have found that pensions do act as a retention incentive, but only for teachers who are very close to reaching retirement age. Once teachers finally reach the retirement age, they face strong financial incentives to retire immediately. Our paper confirmed that states are assuming this as well; they base their financial models on the assumption that the pension plan will exert a strong “push” effect around the normal retirement age that encourages veteran teachers to retire

AFT President Randi Weingarten responded to the report with a three-page press release. We thank Weingarten, and the AFT staff that prepared the response, for reading. Unfortunately, they did not reach out to us before responding, so we have to clear up some errors made in the release. As it stands, there are a number of factual inaccuracies in Weingarten’s response, which I walk through and explain below.

There is an old adage that if a lawyer has the facts on their side, they should pound the facts. If they have the law on their side, they pound the law. And if they have neither, then they should pound the table. Weingarten, an attorney by training, is pounding the table here.

Before I get to the specific errors, you can read our full report here, and we’ve published more detailed methodologies in our reports on teacher turnover rates and break-even points.

Before I get to the specific errors, you can read our full report here, and we’ve published more detailed methodologies in our reports on teacher turnover rates and break-even points.

I’ve published an annotated version of the AFT press release on the Bellwether site, or you can find the original version without our notes here (pdf).

Weingarten: Teachers who vest receive a guaranteed retirement income, and teachers who leave before vesting get all their own contributions back, with interest.

Aldeman: As we show in the paper, only about half of all new teachers vest. Even among those who do vest, the average pension is not that great unless teachers stay in the same state for 25 or 30 years. As we wrote last summer, “The average state pays an interest rate on employee contributions of 3.45%. This is better than the interest on a common savings account today, but it’s about half of what states assume they will earn on their own investments.”

Weingarten: The system provides real retirement security for participants, which the authors want to dismantle.

Aldeman: This is factually untrue, and an ad hominem attack. As our report shows, states assume that only about one out of every five teachers does well under current plans. That’s not merely our assertion — those are the actual estimates state pension plans use to make fiscal decisions. Weingarten may think that arrangement is fine, but it means that roughly four-fifths of teachers are losing out under the current system. And fewer than half of all teachers ever qualify for any pension. We think that’s an unacceptable approach to retirement policy for a field as populous and important as teaching, and it’s disappointing that people who claim to be advocates for teachers don’t also recognize what a retirement security problem this is for millions of American teachers. At Teacherpensions.org we make clear that dismantling teacher retirement is not an adequate response to these problems and also provide analysis about possible alternatives – we do not take a position on a preferred response.

Weingarten also includes a footnote to a study by UC-Berkeley’s Nari Rhee. Rhee’s analysis purposefully ignores early-career teachers—when large proportions of teachers turn over—and looks only at teachers who reach at least five years of service in California. After scrubbing away about one-third of all new California teachers, Rhee finds that about 70 percent of the rest stick around for a full career.

In contrast, our study looks at all new entrants. I believe that’s a better metric than selectively ignoring such a large group of people. When Rhee’s study came out, I used her own calculations on benefit accruals to show that about half to two-thirds of California’s incoming teachers will fail to break even in their pension system. A follow-up study by Bob Costrell and Josh McGee reached similar findings: About two-thirds of all new California teachers lose out from their pension system.

Weingarten: The median family of retirement age in America has just $12,000 in savings. Half of all Americans have saved less than $24,000 for retirement and half of working Americans— 78 million—work for employers that do not offer a retirement plan. Social Security accounts for 90 percent of retirement income for a third of all recipients and half of retirement income for minorities.

Aldeman: Weingarten is right that many Americans don’t have sufficient retirement savings, but she’s using those stats here in misleading ways. First, she seems to be implying that this is new, and that it was caused by the decline of defined benefit pension systems. But that’s not true at all. Pensions have always been back-loaded, and there was never some sort of golden era of retirement security where everyone had a pension.

But Weingarten’s use of these stats is particularly cynical. Inserting those arguments here amounts to little more than a “Don’t look behind the curtain!” distraction. By changing the conversation to all Americans, Weingarten is trying to avoid a conversation specifically about teacher retirement benefits. She’s done this before. Weingarten also mentions Social Security, which I will say more about in a moment because it’s an issue that adversely affects many teachers.

Weingarten: The assumptions underpinning Bellwether’s report are erroneous. The firm develops its model in a vacuum, where the impact of wages, working conditions, new job opportunities, and family income and responsibilities is suspended, and only pension rules are used to determine whether a teacher vests and when she retires.

Aldeman: This is patently false. We used each state’s own financial assumptions, which are freely available in state financial reports for anyone to download and analyze. In other words, this is not Bellwether’s model or estimate, these are the numbers states and pension plans use to make their own fiscal decisions. Because states are basing their financial estimates about how much money they’ll need to save today in order to pay benefits in the future, they need their assumptions about teacher turnover to be as accurate as possible. In fact, states regularly conduct “experience studies” that look at how their assumptions compare to actual outcomes, which account for wages, working conditions, new job opportunities, etc.

Weingarten The report misrepresents the impact of defined benefit pension plans on those who leave teaching, omitting the fact that there isn’t forfeiture of contributors, and it fails to explain the positive impact of defined benefit pension plans on those who stay. In addition, it tends to ignore the fact that about half of all teachers are excluded from Social Security and therefore rely on the pension as their main source of retirement income.

Aldeman: We’ve written extensively about teachers being excluded from Social Security (the figure is closer to 40 percent nationally), and we think it’s a real problem and believe that enrolling all teachers in Social Security, as a complement to employer-provided retirement benefits, would carry a number of important benefits for teachers. We’re happy to see the AFT acknowledge the issue, but historically it has been union opposition that has kept Social Security voluntary for state and local governments.

Weingarten: Furthermore, Bellwether’s state pension fund sample includes several funds that have commingled data for a variety of employees, making it impossible to separate teachers from other education employees. Teachers have an average turnover rate much lower than noncertificated employees, and higher average years of service.

Aldeman: We used each state’s assumptions for teacher turnover rates, and it’s true that in some states the teacher rates are commingled with other types of workers. But we didn’t find any state that assumed its vesting period served as a retention incentive, regardless of whether or not they grouped teachers with other types of workers or not.

Moreover, AFT often represents non-certficated education employees in addition to teachers. It’s alarming that they don’t seem to care equally about the retirement security of all their members. Regardless, as a public policy, we shouldn’t design systems that systematically disadvantage large groups of workers.

AFT then responds to the four recommendations in our paper:

Weingarten: Lowering vesting standards to no more than three years… would provide an incentive for more teachers to leave the profession earlier rather than later.

Offering graded vesting… also provides an incentive to leave early and hurts taxpayers.

Aldeman: Our analysis of state pension plan data suggests that vesting is not currently an incentive for teachers, and AFT has not refuted that central finding. Until there’s convincing data otherwise, it’s reasonable to say that retirement plans should be for workers, not their employers.

And, while it’s nice to see Weingarten’s concern for taxpayers, her own members are losing out by long vesting periods. Why would a union leader want to make it harder, not easier, for her members to qualify for retirement benefits?

Weingarten: Moving to a more gradual accumulation of benefits. States maintain their pension formulas to account for both productivity gains and inflation over a teaching career, and to provide a meaningful benefit to a career teacher. Other models that base the final benefit on average wages do not provide educators with retirement security, especially for educators in non-Social Security states.

Aldeman: Weingarten’s response here is odd. Our suggestion is for states to shift their formulas so they base pension amounts over more years of service, rather than just three or five as is common today. That would have the effect of smoothing out pension benefit accrual and making them fairer to younger workers (pension formulas currently value years of service earned closer to retirement than those earned further in the past). This would make pensions function more like Social Security, which bases its benefits off of 35 years of earnings and adjusts earlier years for inflation. No state does this for its teachers, but it’s a good model, and it’s one reason that Social Security provides a solid, progressive base of benefits for all workers.

Weingarten: Not using pension plans to help retain teachers. Pension policy and design can and should follow a workforce policy that is aimed at attracting and retaining a high-quality workforce for the long term.

Aldeman: I agree with the intent here, but Weingarten is not engaging with the research base on pensions. Several studies have found that pensions have a small back-end retention effect, but it comes too late to affect the retention patterns for most teachers. Moreover, researchers have found that pension plans’ large push-out effect, where veteran teachers are effectively pushed to retire, harms student outcomes. If we want more outstanding veteran teachers in the classroom we should make sure they are not incentivized to retire when they still have more to give and that schools are not working at cross-purposes with retirement schemes in their efforts to retain these teachers.

Chad Aldeman is a principal at Bellwether Education Partners

This post originally appeared at BellwetherEducation.org.