A great deal has changed since March 2020, when executive and Congressional action paused payments on most federal student loans. The national unemployment rate spiked at 14.7 percent in April 2020, but receded dramatically and has stayed below 4 percent since December of 2021. Meanwhile, inflation climbed from an average of 1.2 percent in 2020 to 9.1 percent in June 2022—the biggest jump in 40 years.

Yet, following nine extensions, the payment pause on student loans remains in place at an approximate direct cost of $5 billion per month. The Biden Administration also has moved to end some repayments altogether, by forgiving hundreds of billions of dollars in federal student loans. Whether the forgiveness program is legal, and whether millions of Americans will have to repay their student loans back in full, is now before the U.S. Supreme Court. Justices will hear the case on February 28.

These two policies may be tethered to one another in court, but they have strikingly different distributional impacts. While the White House claims that nearly 90 percent of the relief provided under the forgiveness plan would go to families with incomes less than $75,000, the payment pause has provided more than 65 percent of the relief to families with incomes greater than $75,000. In fact, the top 20 percent of households receive nearly 30 percent of the benefit while only accounting for 16 percent of families with federal student debt.

We look at the household student loan balances, payments, as well as earnings, to determine the relative impacts of the payment pause program on lower- and higher-income Americans. Our analysis shows the across-the-board pause on federal student loan payments disproportionately benefits the most affluent borrowers. Continuing the payment pause without means-testing its benefits leads to ballooning costs for taxpayers.

Still, in the absence of some payment relief, approximately 12 percent of families, who disproportionately have low and moderate incomes, have payment-to-income ratios greater than conventional metrics for excessive student debt burden. If both the payment pause and promise of partial loan forgiveness end with an adverse Supreme Court ruling in early 2023, these borrowers are at risk of significant negative financial impacts.

The reliance on the payment pause may have made other avenues of relief, including relief under Income-Driven Repayment plans and the Fresh Start program, less salient for the most vulnerable borrowers. Yet these more stable avenues represent the best way to assist borrowers most in need of government support. Encouraging families to seek out these options now, while the pause is still in effect, is an important safeguard for borrowers’ longer-term financial health.

How Much does the Student Loan Payment Pause Cost?

Various government sources and independent policy organizations have provided cost estimates to the student loan payment pause. Reconciling these estimates requires articulation of the impact of the payment pause on the federal budget along with other economic indicators.

Available government measures have recorded the pause on financial statements as “loan modifications,” which is essentially the cost of forbearance with zero interest accrual. The U.S. Department of Education has calculated these costs at $41.9 billion for Fiscal Year 2020 and $53.1 billion for Fiscal Year 2021. The total indefinite appropriations provided in Fiscal Year 2020 and Fiscal Year 2021 for student loan payment deferrals was $98.4 billion. The Congressional Budget Office estimated the cost of the payment pause at $112.8 billion from March 2020 to May 2022. A subsequent letter from the office projected that the 4-month extension of relief from August 2022 to December 2022 would cost an additional $20 billion.

In July 2022, the Government Accountability Office analyzed data from the Department of Education and found that costs associated with the emergency relief between March 2020 and April 2022 totaled $102 billion. This analysis, which does not include extensions beyond August 2022, only measures costs associated with the Direct Loan program and likely underestimates the total cost of the payment pause.

Analysts in the private sector also have considered factors beyond the direct cost of lost interest payments. In August 2022, the Committee for a Responsible Federal Budget (CRFB), a private think tank focused on fiscal policy, estimated the total cost of the pause through the end of 2022 to be $155 billion. With the extension announced in November, the organization presented the cost of the extension of the payment pause until August 2023 as generating a cumulative policy cost of $195 billion. Broadly, the analysis asserts that the pause of collections on loans, interest, and defaults costs $5 billion per month, which is generally consistent with estimates from the Congressional Budget Office.

While government analyses focused more exclusively on the accounting costs of the policy, CFRB also identified the inflationary implications of the pause. First, inflation generates a cost in the erosion of the value of future payments to the government; for individual debt holders, this cost is a “benefit” in the form of reductions in the real value of future payments. Second, as borrowers have more cash-on-hand for consumption, it is likely that the student loan pause increases inflation, with the organization estimating an effect of about 20 basis points per year. Indeed, this inflation impact was acknowledged by the Biden White House, as Council of Economic Advisors member Jared Bernstein claimed that the restarting of student loan payments would offset any inflationary impact of debt forgiveness.

One final component of “cost” that most analyses do not consider is the payments that will be foregone for borrowers receiving Public Service Loan Forgiveness and Income-Driven Repayment forgiveness. For borrowers covered by these programs, the months of forbearance during the payment pause (34 to date) are included as part of the repayment count. Thus, a worker covered by the public service program, which forgives loan balances after 120 qualifying months of payments, would need only 86 additional qualifying payments to qualify for full loan relief. While it is difficult to provide a full accounting of the eventual “costs” of these forgone payments to the government, they are not distributionally neutral because those borrowers who forego relatively large payments or would have paid off their loans before forgiveness are the largest beneficiaries.

Distributional Evidence

The benefits of the payment pause tie directly to the balances, monthly payments, and the interest rates on the loans. Each of these components contributes to the net regressive impact of the payment pause continuation.

Interest rates on federal student loans vary based on the education level of the borrower and the type of loan, effectively representing the current benefit per dollar borrowed. To illustrate, for 2022, the interest rate for undergraduate borrowers is 4.99 percent, while graduate borrowers face a rate of 6.54 percent. Through the PLUS program, graduate and professional students who borrow beyond the basic limit and parents borrow at 7.54 percent interest. Thus, for each dollar borrowed, PLUS borrowers receive the greatest “benefit” from the pause.

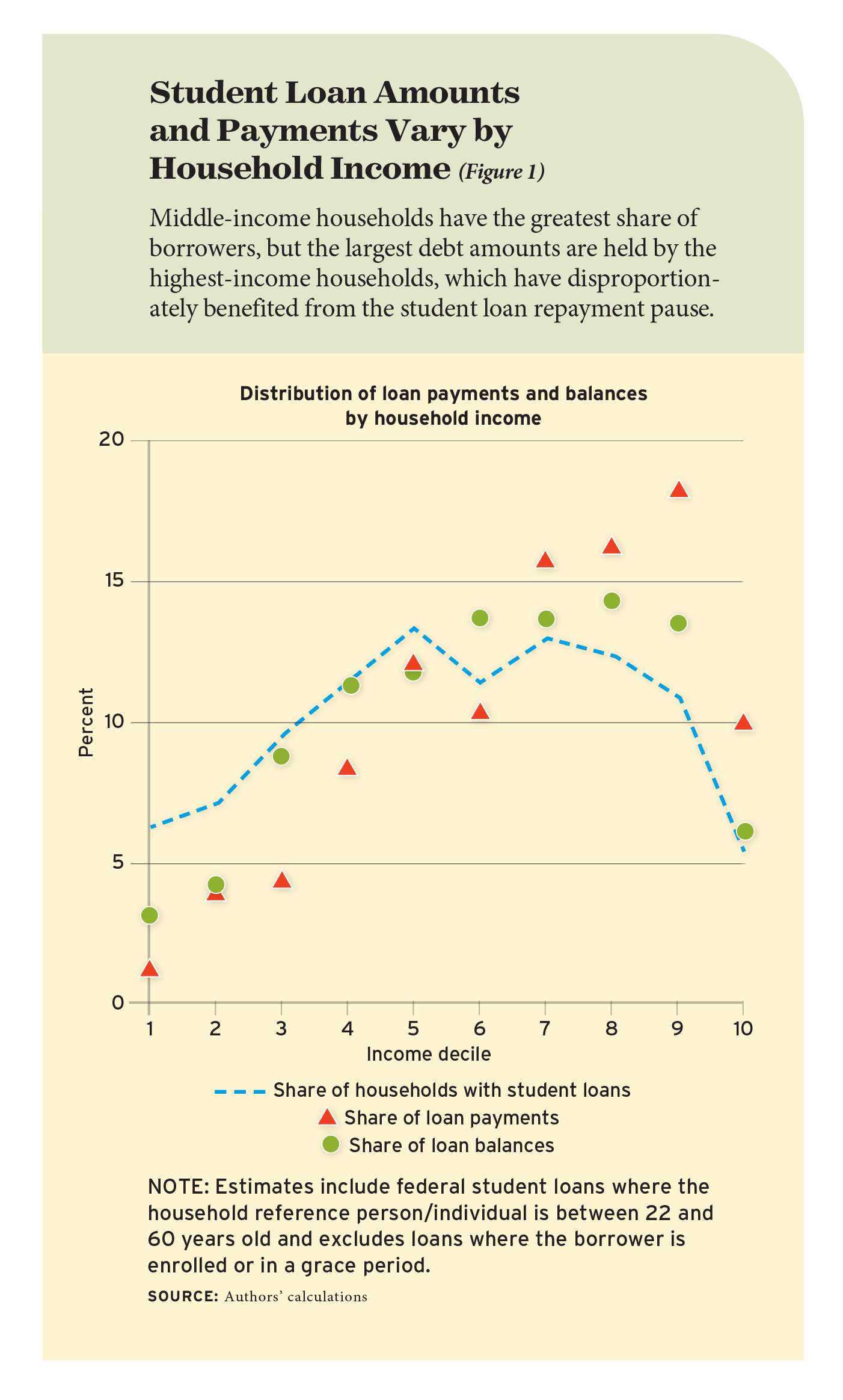

Using data from the 2019 Survey of Consumer Finances, we organize households with federal student debt (our sample of ”borrowers”) by decile of family income to estimate the distribution of student loan payments and balances. While the incidence of borrowing is broadly concentrated in the middle of distribution (about 71 percent in the middle 60 percent of the distribution), both payments and balances are concentrated in the top part of the income distribution (see Figure 1). Borrowers in the top four deciles, with approximate family incomes greater than $80,000, account for about 47.4 percent of student loan balances and about 60 percent of student loan payments, but only 41.4 percent of households with federal student debt. The greater concentration of student loan payments (relative to balances) in the top deciles reflects the fact that borrowers at lower deciles are more likely to be in deferment or enrolled in income-based repayment.

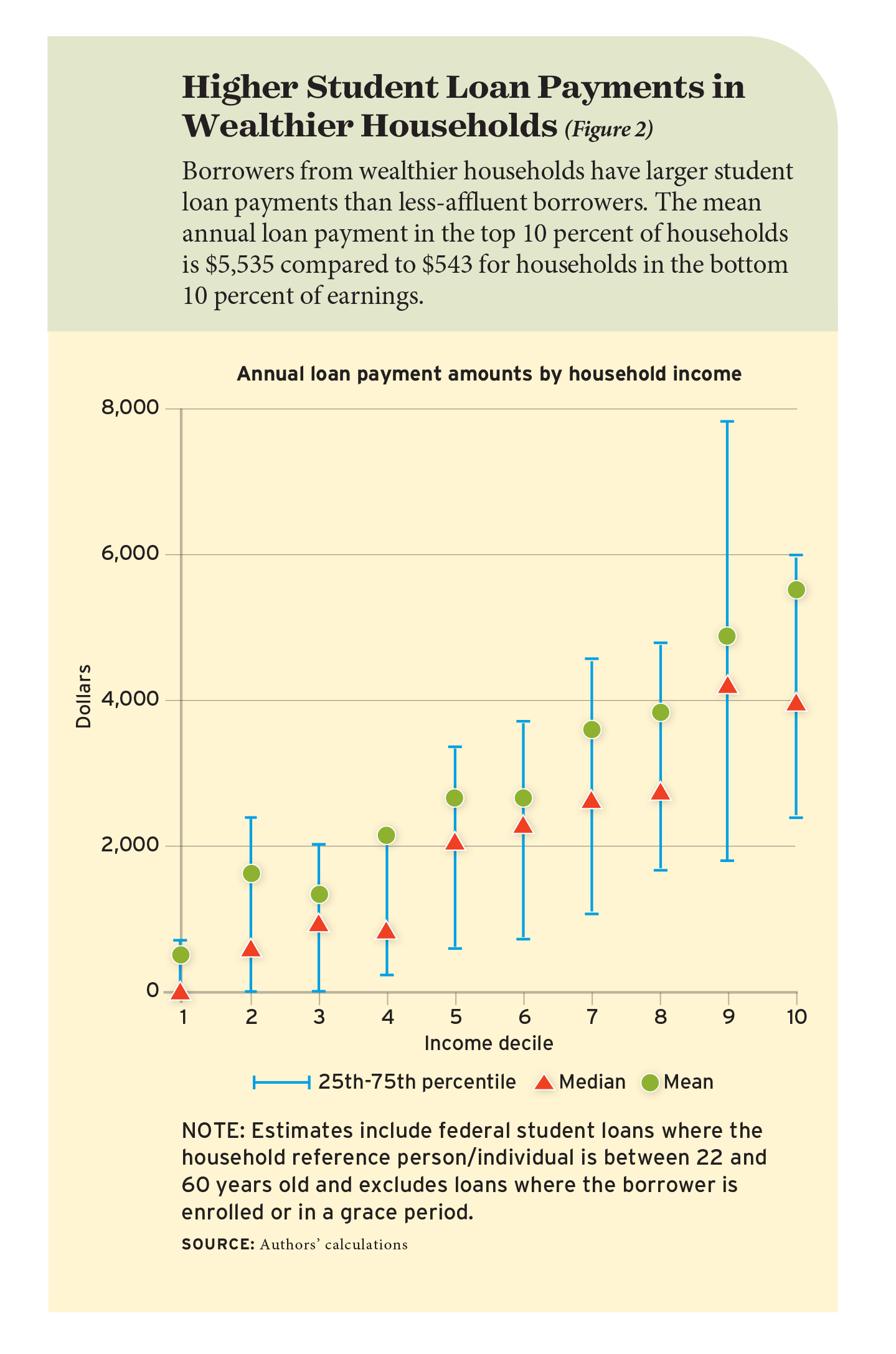

We also see an upward march of mean loan payments across the income distribution, making clear that higher-income households see the largest increases in cash-on-hand and interest subsidies from the payment pause (see Figure 2). What is more, the erosion of the real value of future liabilities with high inflation (4.7 percent in 2021 and 8.0 percent in 2022) disproportionately benefits high-balance borrowers, who are likely to be found in the top deciles of the income distribution.

The payment-income patterns we observe also have been documented in administrative banking data linked to credit reports. Research published by the JPMorgan Chase Institute, for example, examines an extraordinarily rich dataset involving 301,000 people. It demonstrates that for borrowers making about $30,000 per year, the median monthly payment is about $134 and the 90th percentile payment about $419; for borrowers making about $130,000 per year, the median monthly payment is about $225 and the 90th percentile payment about $813.

Even as payments and loan balances, along with interest premiums, are skewed to the top part of the income distribution, the question of how the “burden” of student loans is measured relative to income merits investigation. We therefore also plot the means of student loan payment to income ratios by household earnings decile.

Mean payment-to-income ratios generally decline with income and range from approximately 1.8 percent in the top decile to 6.3 percent in the 2nd decile. However, there is notable variation in the degrees of burden both overall and within income deciles, even as these ratios tend to be higher at the bottom than at the top of the income distribution. In total, 12 percent of families have payment-to-income ratios greater than 8 percent, which is a conventional metric for excessive debt burden. Within deciles, the shares of families carrying an excessive debt burden range from 2.7 percent for the 10th to 27.3 percent for the 2nd. Again, this resembles the patterns observed in the banking data, which show that about one-quarter of borrowers have a scheduled student debt burden above 7.3 percent, while 10 percent is obligated to pay at least 13.3 percent of their take-home pay. The takeaway is that while the majority of borrowers have “manageable” student debt, there is a significant minority that is likely to struggle with repayment.

We also look at which types of degree holders have the highest payment levels. Our analysis shows that nearly 48 percent of payments are made by graduate degree recipients, even as this highly educated group constitutes about 29 percent of borrowers. Finally, we examine borrowing, debt levels, and payments by race. While Black Americans constitute roughly 20 percent of households with federal student loans and hold 23 percent of balances, they make approximately 15 percent of the aggregate loan payments. By contrast, white American households make up about 61 percent of borrowers and 70 percent of payments. Thus, the relief afforded by the payment pause is racially disparate in its absolute impact.

Policy Alternatives

Continuing to extend the student loan payment pause is expensive and regressive. It costs at least $5 billion per month and delivers the bulk of the benefits to upper-income families. In addition, these many extensions threaten the government’s future credibility to administer student loan programs or, indeed, any government lending initiative. With at least three announcements of a “final” pause, it seems unlikely that borrowers will take such announcements seriously and change their spending behavior to prepare for payments to restart. These individuals may face serious financial deficits if payments ever do resume—and the biggest risks are concentrated among families at the lower end of the income distribution. Looking farther in the future, the “normalization” of payment suspension may create an expectation that all forms of perturbations in the economy will be met with a payment pause. Such expectations would make a student lending policy fiscally unsound.

Still, there are plainly borrowers who are at risk of delinquency or default with a resumption of payments. Is extending the payment pause a lifeline for these struggling borrowers, or a diversion that may actually them?

The extension of the payment pause may encourage a false expectation for borrowers. The latest pause announcement claims: “The extension will alleviate uncertainty for borrowers as the Biden-Harris Administration asks the Supreme Court to review the lower-court orders that are preventing the Department from providing debt relief for tens of millions of Americans.” And U.S. Secretary of Education Miguel Cardona introduced the most recent extension of the payment pause by saying:

“Callous efforts to block student debt relief in the courts have caused tremendous financial uncertainty for millions of borrowers who cannot set their family budgets or even plan for the holidays without a clear picture of their student debt obligations…”

It would be difficult to deny that there is uncertainty surrounding the eventual likelihood of debt forgiveness. However, rhetoric from Secretary Cardona and the Department of Education that encourages a false sense of security about the likelihood of debt forgiveness may make at-risk borrowers worse off. Without taking on the role of legal odds-maker, debt forgiveness is far from certain, and a ruling from the Supreme Court against executive action could lead to a payment restart in the first half of 2023 rather than in August 2023. Rather than providing false assurances about the prospects for forgiveness, shouldn’t the Department of Education and the Biden administration be taking every possible step to ensure that borrowers have access to the safety net of resources designed to help those who may struggle with the restart of payments?

Public conversation about student loan forgiveness sometimes invokes a false dichotomy: endlessly continuing the payment pause as the sole alternative to financial ruin for borrowers who are struggling in the labor market or who have been victims of predatory institutions. However, these borrowers have clear options. Indeed, notable accomplishments of the Biden administration include progress to increase access to Income-Driven Repayment, Fresh Start to Repayment, Public Service Loan Forgiveness, and Borrower Defense to Repayment.

Most notably, existing income-based repayment programs are designed to provide relief for low- and moderate-income borrowers for whom standard repayments would cause financial hardship. These programs limit payments based on earnings and eventually forgive outstanding balances after 20 or 25 years. For example, current programs like Pay As You Earn and Revised Pay As You Earn generally cap payments at 10 percent discretionary income. Yet, since the pandemic began, the number of borrowers in income-based repayment programs has increased only slightly, even as it is widely recognized that there are many more borrowers who would benefit but are not enrolled.

The most constructive action from the White House and the Department of Education would be to use the remaining time of the pause to motivate enrollment in existing income-based repayment plans and other programs already “on the books” to help borrowers. Aggressive focus on the politically and judicially uncertain debt forgiveness makes other programs that could provide certain relief less salient to borrowers. Indeed, one hypothesis is that low take-up of the Public Service Loan Forgiveness waiver, which has been suspended as of October 31, 2022, was driven by many borrowers’ expectations that they would be able to get loan relief through forgiveness without having to complete the paperwork filings associated with the public service program.

The political and public relations efforts around the forgiveness plan would appear to crowd out more general outreach and troubleshooting to ensure that at-risk borrowers are protected when payments resume. While more than $100 million was budgeted for the rollout of the forgiveness application, there has been no comparable expenditure to increase take-up of existing loan relief programs for at-risk borrowers. And recent Congressional action, which can be seen as a partisan response to the forgiveness effort, denied additional funding to the Office of Federal Student Aid in the December 2022 omnibus spending bill, exacerbating the problems of antiquated processes and limited trouble-shooting tools. In addition, expending the limited bandwidth of the Department of Education and its Office of Federal Student Aid on an uncertain forgiveness effort or a new income-driven repayment plan with questionable distributional implications seems ill-advised.

Executive action combined with judicial intervention in the student loan space seems to yield short-term and unsustainable fixes. These may not only confuse borrowers, but also contribute to instability in the policy process and, ultimately, the higher education market. If only executive action and judicial decision-making prevail over the course of the next two years, there is no certainty in outcomes. Instead, borrowers are faced with a decision tree of various scenarios reflecting possible combinations of Supreme Court rulings and executive action. Regardless, plausible scenarios including extending the student loan payment pause indefinitely by executive action or ending it by judicial ruling would not address the structural problems of design and implementation that have long plagued federal student lending.

While the legislative process presents significant challenges with razor-thin majorities in both the Senate and House of Representative, looking over the longer term it’s clear that compromise is imperative to build a well-functioning student loan system. Americans need a student loan program that enables the kind of post-secondary investments that contribute to economic prosperity and innovation while also providing borrowers with insurance against weak economic outcomes and oversight to prevent abuse by predatory institutions. In the meantime, the tools exist to protect at-risk borrowers right away: it’s time to put them to use.

How We Got Here: A Brief History of the Student Loan Repayment Pause

The student loan payment pause began March 13, 2020, when President Trump used executive authority to waive interest on all government-held student loans, effectively allowing penalty-free forbearance. The initial presidential announcement did not cite specific authorizing language, though the declaration of the Covid-19 pandemic provided a broad rationale.

When Congress passed the Coronavirus Aid, Relief and Economic Security Act, it included language that required the U.S. Secretary of Education to suspend payments on designated student loans until September 20, 2020. These provisions were not extended by Congress in the summer of 2020; however, President Trump used executive action to direct then-Secretary Betsy DeVos to extend the payment pause until the end of the year. He then issued a payment pause extension to January 31, 2021. These actions cited the Higher Education Relief Opportunities for Students Act of 2003, known as the HEROES Act, which amended the Higher Education Act of 1965 to provide executive authority to “grant waivers or relief” to recipients of federal financial aid in connection with “a war or other military operation or national emergency.”

The use of the HEROES Act to pause student loan payments in 2020 went unchallenged. But a larger question emerged: did the HEROES Act also provide executive authority to cancel student loan debt? Loan forgiveness became a campaign issue in the 2020 Democratic primary and presidential elections. For example, Senator Bernie Sanders called for canceling “all student loan debt for the some 45 million Americans who owe about $1.6 trillion.” Senator Elizabeth Warren articulated her call for canceling student loan debt early in her campaign and well before the start of the pandemic, with a plan released in April 2019 calling for “the cancellation of up to $50,000 in student loan debt for 42 million Americans.” On the campaign trail, President Biden presented a plan that limited full debt forgiveness to low- and middle-income borrowers who had attended public institutions or Historically Black Colleges and Universities and then proposed to “immediately cancel a minimum of $10,000 of student debt per person, as proposed by Senator Warren in the midst of the coronavirus crisis.”

As one of his first acts in office on January 21, 2021, President Biden extended the student loan repayment pause using the HEROES Act authority until August 31, 2021. As that date neared, the payment pause was again extended until January 31, 2022, with this billed as the “final” extension. Yet there were two additional extensions, to May 31 and then September 30, 2022—a full two years after the pause was granted by Congress.

Alongside the question of the appropriate duration of the payment pause, the Biden administration faced the larger political (and legal) question of whether to attempt to use the HEROES Act to cancel some student debt. That move came on August 24, 2022, when the administration announced executive action to discharge student debt and a “final” extension of the payment pause until December 31, 2022. The plan was soon challenged in court, with two lawsuits effectively halting the program.

The application for student loan forgiveness opened on October 17, 2022. Four days later, the U.S. Court of Appeals for the 8th Circuit placed a temporary hold on the program. During this time the government continued to encourage applications but did not discharge loans. However, on November 10, a federal judge in Texas blocked the loan forgiveness policy and the U.S. Court of Appeals for the 8th Circuit followed with a 3-0 decision granting an order of injunction halting the proposed debt relief plan on November 14. The Biden Administration stopped accepting applications for loan forgiveness on November 11. Beginning on November 19, the Biden administration notified many borrowers who had applied through the Department of Education website that “[Your] application is complete and approved, and we will discharge your approved debt if and when we prevail in court.”

The legality of the forgiveness program will be before the U.S. Supreme Court in February. Justices rejected two early requests to block loan forgiveness but then agreed to hear the case from the Court of Appeals. Meanwhile, the Court of Appeals for the 5th Circuit declined to overturn the Texas judge’s ruling that forgiveness is unlawful, which essentially vacated the program.

With forgiveness suspended and the resumption of payments approaching, an announcement on November 22 extended the student loan repayment pause again. Now payments are scheduled to resume no later than 60 days after June 30, 2023, giving time for the Supreme Court to consider the case.

While there were few questions about the legal status of the payment pause at the height of the Covid-19 pandemic, questions about the legality, cost, and distributional implications of the extension have received greater scrutiny. The legal questions, as summarized by a 2021 Congressional Research Service report, involve the interpretation of the language of the HEROES Act, the process of its implementation, and whether a “national emergency” remains in effect. The legal standing of payment pause extensions under the HEROES Act is not unassailable, but this is ultimately a question for the courts. That said, there are notable parallels with the 2021 U.S. Supreme Court decision in Alabama Association of Realtors v. Department of Health and Human Services, which struck down the continuation of a moratorium on evictions from executive action rather than the legislative process.

Diego Briones is a doctoral candidate in economics at the University of Virginia. Eileen Powell is a graduate student at the Batten School of Leadership & Public Policy at the University of Virginia. Sarah Turner is University Professor of Economics and Education and Souder Family Professor at the University of Virginia.

This article appeared in the Summer 2023 issue of Education Next. Suggested citation format:

Briones, D., Powell, E., and Turner, S. (2023). Student Loan Payment Pause Benefits High-Income Households the Most: With forgiveness uncertain, struggling borrowers are unprotected from risk. Education Next, 23(3), 40-47.

For more, please see “The Top 20 Education Next Articles of 2023.”